What kind of income is allowed and needed for a FHA, VA, USDA and Fannie Mae Mortgage Loan Approval in Kentucky?

Income and your job history plays a significant role when applying for a mortgage loan and getting approved for one for Kentucky Homebuyers . Mortgage Underwriters from FHA, VA, USDA and Fannie Mae must follow both Fannie Mae and agency guidelines when it comes to documenting and calculating qualifying income for a loan transaction. Income guidelines may vary slightly depending on the loan program and the borrower’s employment profile. Below are some general tips for W2 income.

Documentation that may be required

Paystub with year to date gross earnings

At least 1 year’s W2

Verbal or full VOE

Base Pay

Salaried and fixed hourly income is calculated by averaging the gross year to date income

Variable hourly income is calculated by averaging 12 month history

Commission and tip income is calculated by averaging over 24 months

No transcripts are required for salaried, hourly, or less than 25% commission W2 income borrowers

Unreimbursed expenses do not have to be deducted from the gross pay for salaried, hourly, or less than 25% commission W2 borrowers

Overtime, and Bonus Income

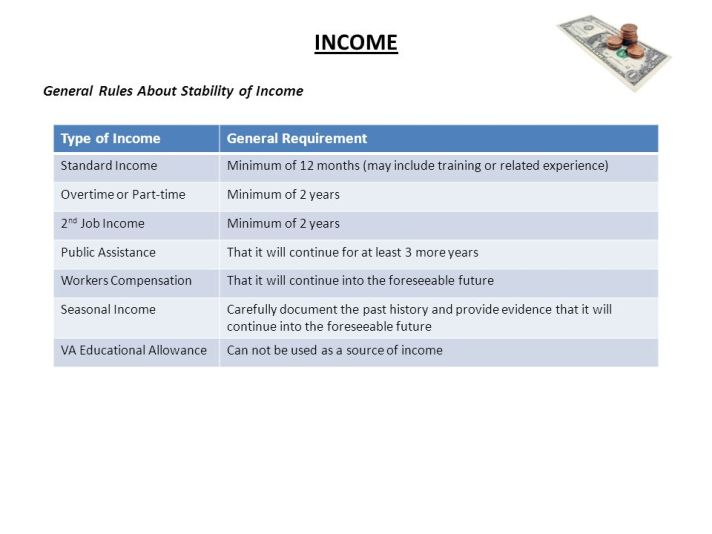

Overtime and Bonus can be used as effective income as long as it’s been received for 2 years and is reasonably likely to continue

Periods of less than 2 years may be considered as long as it’s been consistently earned over a period of at least 12 months and there are positive factors to offset the shorter history of receipt per underwriter discretion

Overtime and Bonus income must be documented by a full VOE

Declining overtime and bonus income cannot be used for qualifying income

Part Time Income

FHA requires a 2 year history of working multiple jobs

Fannie will allow less than 2 years as long as it’s been consistently earned over a period of at least 12 months and there are positive factors to offset the shorter history of receipt per underwriter discretion

All loans and lines are subject to credit approval, verification, and collateral evaluation and are originated by lender. Products and interest rates are subject to change without notice.

The view and opinions stated on this website belong solely to the authors, and are intended for informational purposes only. The posted information does not guarantee approval, nor does it comprise full underwriting guidelines. This does not represent being part of a government agency. The views expressed on this post are mine and do not necessarily reflect the view of my employer. Not all products or services mentioned on this site may fit all people.

NMLS ID# 57916, (www.nmlsconsumeraccess.org).

Reblogged this on Kentucky FHA Mortgage Loans Guidelines and commented:

What kind of income is allowed and needed for a FHA, VA, USDA and Fannie Mae Mortgage Loan Approval in Kentucky?

LikeLike