About

Documents Needed for a Mortgage Loan Approval

What is a Kentucky Mortgage Rate Lock?

Fannie Mae HomePath Ky

Glossary

Homeownership: Kentucky

Kentucky Mortgage Calculators

Kentucky Rural Housing USDA Loans

Kentucky VA Mortgage Frequently Asked Questions

Louisville Kentucky Down Payment Assistance Mortgage Program

Tips to ensure your mortgage closes smoothly

What not to do After You Apply for a Mortgage Loan Approval

Accessibility Statement

First-Time HomeBuyer Louisville Kentucky Mortgage Programs

Kentucky First Time Home Buyer Questions and Answers

Kentucky Housing Corporation (KHC)

Credit Scores for Kentucky Mortgages

Credit Scores Needed To Qualify For A Kentucky Mortgage Loan Approval?

Debt-to-Income Ratio for Kentucky Mortgage Loans:

Kentucky FHA Loan Louisville Kentucky Mortgage Guidelines

Kentucky FHA loan requirements

Kentucky FHA credit score minimums

500, with 10% down

580, with as little as 3.5% down

Kentucky FHA down payment minimums

3.5% down, a credit score 580 or above. This requires you to pay mortgage insurance premiums for the life of the loan.

10%, down, if your credit score is 500 to 580. You must pay mortgage insurance premiums for 11 years.

Kentucky FHA loan limits

FHA loans come with limits, but there’s no standard amount across the country. Instead, the limits vary by county and are adjusted on an annual basis. In 2023, the maximum FHA loan amount you could borrow ranged from $472,030

2023 Kentucky conforming and FHA loan limits are $472,030 for a one unit property

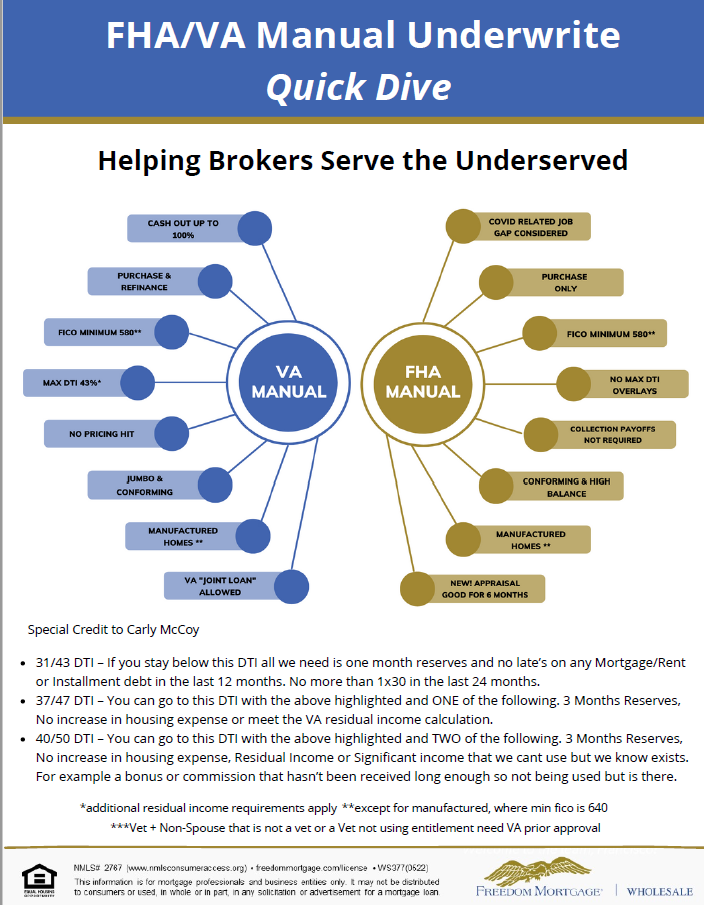

Kentucky Max FHA DTI Debt to Income Ratios maximum

You typically must have a debt-to-income ratio of 56.9% or lower on an Approved Eligible File through AUS on the Front back end ratio and the front end debt ratio is usually limited to 45% on the front end.

On FHA manual underwrites, the max debt ratio are as follows:

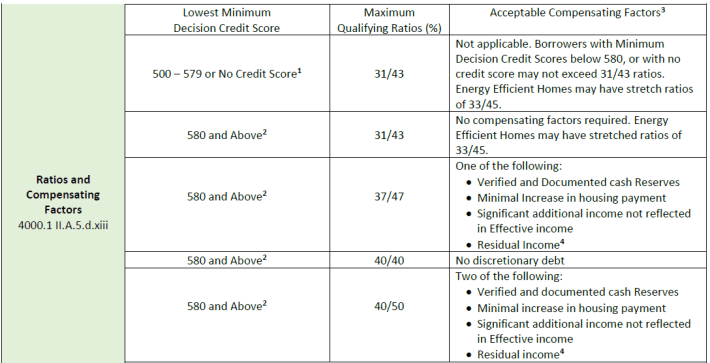

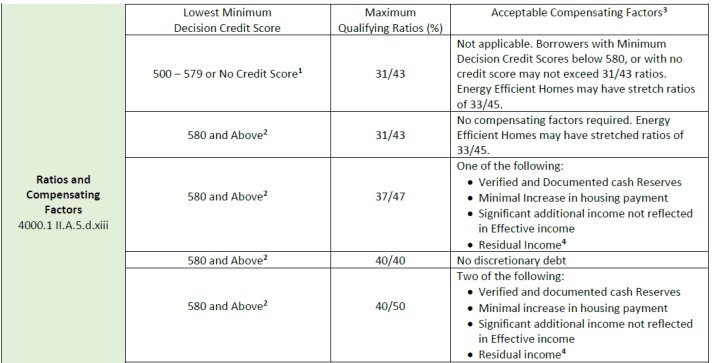

KENTUCKY MORTGAGE GUIDELINESKENTUCKY MORTGAGE GUIDELINES FOR A MANUAL UNDERWRITE AND CREDIT SCORE AND DEBT RATIO REQUIREMENTS WITH DOWN PAYMENT

Qualifying Ratios (%)

Acceptable Compensating Factors

500 – 579 or No Credit Score1

31/43

Borrowers with Minimum

Decision Credit Scores below 580, or with no

credit score may not exceed 31/43 ratios.

580 and Above2

31/43

No compensating factors required. Energy

Efficient Homes may have stretched ratios of

33/45.

580 and Above2

37/47

One of the following:

• Verified and Documented cash Reserves

• Minimal Increase in housing payment

• Significant additional income not reflected

in Effective income

• Residual Income4

580 and Above2 40/40 No discretionary debt

580 and Above2

40/50

Two of the following:

• Verified and documented cash Reserves

• Minimal increase in housing payment

• Significant additional income not reflected

in Effective income

FHA KENTUCKY loan requirements for Job and Income

Show proof of income and an employment history of at least two years

Purchase a home that you’ll use as your primary residence

Get the property appraised by an FHA-approved appraiser and make sure it meets HUD guidelines

Not have a history of bankruptcy or foreclosure in the past year for Chapter 13 and 2 years removed from Chapter 7 and no foreclosures in last 3 years

KENTUCKY MORTGAGE GUDIELINES FOR BANKRUPTCY, SHORT SALE, FORECLOUSRE, CHAPTER 13 AND CHAPTER 7

FHA costs: mortgage insurance

FHA loans often come with attractive interest rates, as a result of their government guarantee. But you should expect your savings to be at least partially offset by extra costs in the form of mortgage insurance premiums, which are designed to cover costs if you default on the loan.

If your down payment is 10%, you’ll pay these premiums for 11 years. Otherwise, you’ll be stuck paying them until you sell your home or refinance your mortgage.

Here’s what the upfront and annual mortgage insurance premiums typically cost:

Upfront mortgage insurance premium: 1.75% of your loan amount

Annual mortgage insurance premiums: 0.45% to 1.05% of your loan amount, depending on your term and other factors

KENTUCKY MORTGAGE GUDIELINES FOR BANKRUPTCY, SHORT SALE, FORECLOUSRE, CHAPTER 13 AND CHAPTER 7

KENTUCKY MORTGAGE GUDIELINES FOR BANKRUPTCY, SHORT SALE, FORECLOUSRE, CHAPTER 13 AND CHAPTER 7