Credit Scores are important for getting approved for a Mortgage in Kentucky.

Below I have spelled out some info that will help you out when you look at your credit scores and what affects them and what you can do to help your credit scores in order to prepare for a mortgage loan approval when it comes to your credit scores.

- Opting out will help a credit score.

No it won’t. The bureaus don’t know if someone has opted out or not and it’s not factored into the credit scores. If someone’s score improves after they have opted out it’s because something else has changed on the report but not because they opted out. - Paying off old delinquencies will remove them from your credit report.

No a collection account or an account with late payments will stay on a credit report for 7 years. That being said, the credit bureaus will occasionally go in and remove old collections that have not reported for a while. But that’s at their discretion. Just because you paid if off doesn’t mean it will be removed. Also paying off an older collection with then brings the reporting date current which could actually hurt the credit scores. - All rate shopping inquiries are the same.

If you are rate shopping for a mortgage or auto, all inquiries with Trans Union and Equifax have a 45 day window. For Experian however it’s only 15 days. For revolving inquiries there is no “shopping” period. All those inquiries are counted no matter what the time frame is. - Opening new accounts will help your credit score.

This will help only if the borrower has no established credit yet. Once you have several accounts, opening new ones will actually have a negative affect on a credit score until substantial history is accumulated on the account. - Paying off all your revolving balances is a good thing!

Actually no it’s not. The credit bureaus models like to see at least one revolving balance, even if it’s small. Having no revolving balances can actually have a negative impact on a credit score. So always keeping one account with a small balance is a very good idea. - Your credit is affected by how much money you have in your savings or checking accounts.

Neither of these are factored into a credit score. - Closing old accounts will help a credit score.

The credit scoring models like to see several open accounts that have zero balances and are not used often. When an account is closed you lose that history. If it’s an account you’ve had for a long time and has no late payments, closing it can actual hurt the credit score. Having several open accounts, even if they are not used much, makes it look like a person has good financial responsibility. - When I check my own credit score it’s the same one used by lenders.

Unfortunately no it’s not. A person actually has 69+ different credit scores. The ones that lenders use are completely different than what a borrower sees when they get their own scores. Those are personal scores and are not used by any industry for any reason. - Checking my own credit report will hurt my score.

When a consumer checks their own credit report it’s a “soft” inquiry and will not impact the scores. Only “hard” inquiries done by creditors when a consumer applies for a loan or credit card will possibly have a negative affect on a credit score.

It’s possible to avoid paying for your credit score or at least an estimate. Here is a list of all of the well-known ways to get a FICO score or score estimate for free:

Free FICO credit scores:

- Discover Free Credit Scorecard (Experian, FICO-08)

- freecreditscore.com (Experian, FICO-08) — you do not need to give your credit card number

For free estimates of your credit score estimates and credit monitoring:

- Credit Karma (TransUnion, Equifax)

- Credit.com (Experian)

- Mint (Equifax)

- Chase Credit Journey (TransUnion)

Also see the Wikipedia page on free credit report websites.

Credit cards (no annual fee) that offer a free FICO score with their monthly statement or online:

- Amazon Synchrony Store Card (TransUnion, FICO-08)

- American Express (Experian, FICO-08)

- Bank of America Cards (TransUnion, FICO-08)

- Barclaycards including the Sallie Mae Mastercard (TransUnion, FICO)

- Branded Citibank cards (Equifax, FICO-08)

- Chase Slate (Experian, FICO)

- Discover cards (Transunion, FICO-08)

- FNBO Cards (Experian, FICO-08 Bankcard)

- Walmart Store Card (TransUnion, FICO)

- Wells Fargo Cards (FICO)

Deposit accounts that offer a free FICO score with their monthly statement:

- Digital Credit Union (EQ-05: Mortgage Score)

Credit cards (no annual fee) that offer a free estimated credit score online:

- Capital One credit cards (TransUnion, VantageScore 3.0)

Note that score ranges vary between FICO scores and other scores:

- FICO: 300 to 850 (used in 85-90% of credit decisions)

- VantageScore (used in 10-15% of credit decisions)

- VantageScore pre-3.0: 501 to 990

- VantageScore 3.0: 300 to 850

- TransUnion New Account Score: 300 to 850 (score estimate)

- Equifax: 280 to 850 (score estimate)

- Experian: 330 to 830 (score estimate)

—

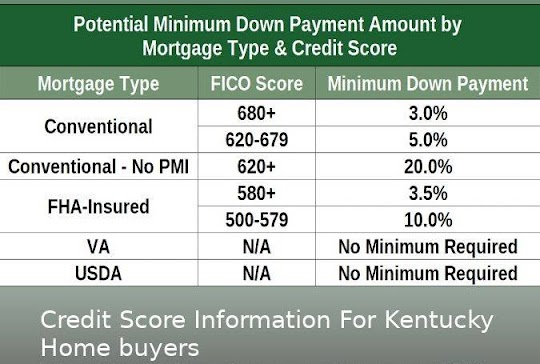

Credit score used for a Kentucky Mortgage Loan Approval for FHA, VA, USDA Rural Housing, KHC Down payment assistance FAnnie Mae

Joel Lobb Mortgage Loan Officer NMLS 57916

EVO Mortgage

911 Barret Ave, Louisville, KY 40204

Company NMLS ID # 173846

Text/call: 502-905-3708

email: kentuckyloan@gmail.com

http://www.mylouisvillekentuckymortgage.com/

NMLS 57916 | Company NMLS #173846

The view and opinions stated on this website belong solely to the authors, and are intended for informational purposes only. The posted information does not guarantee approval, nor does it comprise full underwriting guidelines. This does not represent being part of a government agency. The views expressed on this post are mine and do not necessarily reflect the view of my employer. Not all products or services mentioned on this site may fit all people.

NMLS ID# 57916, (www.nmlsconsumeraccess.org).

Reblogged this on Louisville Kentucky Mortgage Loans and commented:

Credit Report Tips

Credit Reports

credit score

Credit Score First Time Home Buyer Louisville Kentucky KHC

Credit Score Raising it

Credit Scores

Credit Scoresrequired for KHC

LikeLike

Is this information state specific to Kentucky or is it all state’s?

LikeLike