How to Qualify for a Kentucky Mortgage: Income and Employment Guide

Acceptable Income and Job History for a Mortgage Loan Approval in Kentucky

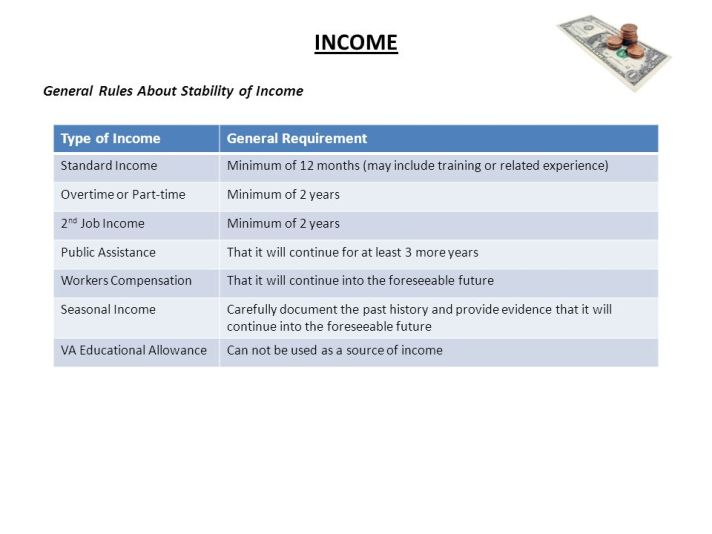

Mortgage Underwriters must follow both DU and agency guidelines when it comes to documenting and calculating qualifying income for a loan transaction. Income guidelines may vary slightly depending on the loan program and the borrower’s employment profile. Below are some general tips for W2 income.

Documentation that may be required

Paystub with year to date gross earnings

At least 1 year’s W2

Verbal or full VOE

Base Pay:

Salaried and fixed hourly income is calculated by averaging the gross year to date income

Variable hourly income is calculated by averaging 12 month history

Commission and tip income is calculated by averaging over 24 months

No transcripts are required for salaried, hourly, or less than 25% commission W2 income borrowers

Unreimbursed expenses do not have to be deducted from the gross pay for salaried, hourly, or less than 25% commission W2 borrowers

Overtime, and Bonus Income:

Overtime and Bonus can be used as effective income as long as it’s been received for 2 years and is reasonably likely to continue

Periods of less than 2 years may be considered as long as it’s been consistently earned over a period of at least 12 months and there are positive factors to offset the shorter history of receipt per underwriter discretion

Overtime and Bonus income must be documented by a full VOE

Declining overtime and bonus income cannot be used for qualifying income

Part Time Income:

FHA loans requires a 2 year history of working multiple jobs

Fannie Mae or Conventional loans will allow less than 2 years as long as it’s been consistently earned over a period of at least 12 months and there are positive factors to offset the shorter history of receipt per underwriter discretion

How to get approved for a Kentucky FHA, VA, USDA and Fannie Mae Mortgage loan with Variable Income

Variable INCOME if your borrower is not hourly at 40 hours a week or salary do you fall within VARIABLE INCOME??

Yup we all dislike that is calculated by an averaging method..

Examples of income of this type include income from hourly workers with fluctuating hours, or income that includes commissions, bonuses, or overtime.

History of Receipt: Two or more years of receipt of a particular type of variable income is recommended; however, variable income that has been received for 12 to 24 months may be considered as acceptable income, as long as the borrower’s loan application demonstrates that there are positive factors that reasonably offset the shorter income history.

Frequency of Payment: us as a lender must determine the frequency of the payment Examples:

If a borrower is paid an annual bonus on March 31st of each year, the amount of the March bonus should be divided by 12 to obtain an accurate calculation of the current monthly bonus amount.

Note that dividing the bonus received on March 31st by three months produces a much higher, INACCURATE monthly average.

If a borrower is paid overtime on a biweekly basis, the most recent paystub must be analyzed to determine that both the current overtime earnings for the period and the year-to-date overtime earnings are consistent and, if not, why.

There are legitimate reasons why these amounts may be inconsistent yet still eligible for use as qualifying income. For example, borrowers may have overtime income that is cyclical (transportation employees who operate snow plows in winter, package delivery service workers who work longer hours through the holidays).

We must investigate the difference between current period overtime and year-to-date earnings and document the analysis before using the income amount in the trending analysis.

Income Trending: After the monthly year-to-date income amount is calculated, it must be compared to prior years’ earnings using the borrower’s W-2’s or signed federal income tax returns (or a standard Verification of Employment completed by the employer or third-party employment verification vendor).

If the trend in the amount of income is stable or increasing, the income amount should be averaged.

If the trend was declining, but has since stabilized and there is no reason to believe that the borrower will not continue to be employed at the current level, the current, lower amount of variable income must be used.

If the trend is declining, the income may not be stable.

Additional analysis must be conducted to determine if any variable income should be used, but in no instance may it be averaged over the period when the declination occurred.

Disclaimer: No statement on this site is a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet Loan-to-Value requirements, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines and are subject to change without notice based on applicant’s eligibility and market conditions. Refinancing an existing loan may result in total finance charges being higher over the life of a loan. Reduction in payments may reflect a longer loan term. Terms of any loan may be subject to payment of points and fees by the applicant Equal Opportunity Lender. NMLS#57916http://www.nmlsconsumeraccess.org/

— Some products and services may not be available in all states. Credit and collateral are subject to approval. Terms and conditions apply. This is not a commitment to lend. Programs, rates, terms and conditions are subject to change without notice. The content in this marketing advertisement has not been approved, reviewed, sponsored or endorsed by any department or government agency. Rates are subject to change and are subject to borrower(s) qualification.

Kentucky Mortgage Approval: Income and Job History Guidelines

Reblogged this on Louisville Kentucky Mortgage Loans and commented:

What kind of income is allowed and needed for a FHA, VA, USDA and Fannie Mae Mortgage Loan Approval in Kentucky?

LikeLike