:root { –ink:#0b1320; –muted:#465066; –brand:#0f766e; –accent:#e6f7f5; –ring:#b8ede7; } .ky-wrap{color:var(–ink);font-family:system-ui,-apple-system,Segoe UI,Roboto,Ubuntu,Cantarell,”Helvetica Neue”,Arial,”Noto Sans”,sans-serif;} .ky-wrap header{padding:2rem 0 1rem;} .ky-wrap h1{font-size:clamp(1.6rem,2.4vw+1rem,2.4rem);margin:.2rem 0 .5rem} .ky-sub{color:var(–muted);margin:0 0 1rem} .ky-badge{display:inline-block;background:var(–accent);color:var(–brand);padding:.35rem .6rem;border-radius:.5rem;font-size:.8rem;border:1px solid var(–ring)} .ky-cta{display:flex;gap:.75rem;flex-wrap:wrap;margin:1.25rem 0} .ky-cta a{text-decoration:none;border:1px solid var(–brand);padding:.65rem 1rem;border-radius:999px} .ky-cta .primary{background:var(–brand);color:#fff} .ky-cta .ghost{background:#fff;color:var(–brand)} .ky-toc{background:#fbfbfc;border:1px solid #edf0f4;border-radius:12px;padding:1rem;margin:1rem 0} .ky-toc a{text-decoration:none;color:var(–brand)} .ky-main h2{font-size:1.4rem;margin-top:2rem} .ky-main h3{font-size:1.1rem;margin-top:1rem} .ky-note{background:#fcfdfd;border:1px dashed #d7e5ec;padding:.9rem 1rem;border-radius:10px;color:#213244} .ky-grid{display:grid;gap:1rem} @media(min-width:860px){ .ky-cols-2{grid-template-columns:1fr 1fr} } table.ky-table{width:100%;border-collapse:collapse;margin:1rem 0} .ky-table th,.ky-table td{border:1px solid #e9edf2;padding:.65rem;text-align:left;font-size:.95rem} .ky-table th{background:#f5f7fa} .ky-infobox{border:1px solid #e3eef0;border-radius:12px;padding:1rem;background:#f9fefe} .ky-imgwrap{border:1px solid #e8eef1;border-radius:12px;padding:8px;background:#fff;margin:1rem 0} .ky-kicker{font-size:.95rem;color:#57627a} .ky-tag a{display:inline-block;margin:.2rem .4rem .2rem 0;font-size:.85rem;color:#1c293b;background:#eff4f7;border:1px solid #dde6ee;border-radius:999px;padding:.25rem .55rem;text-decoration:none} .ky-callout{background:#fff;border-left:4px solid var(–brand);padding:.9rem 1rem;border-radius:8px;border:1px solid #eaf1f2} /* Infograph tiles */ .infograph{background:#ffffff;border:1px solid #e8eef1;border-radius:14px;padding:12px;margin:12px 0} .infograph .kpi-grid{display:grid;grid-template-columns:repeat(auto-fit,minmax(180px,1fr));gap:10px} .infograph .kpi{border:1px solid #e9edf2;border-radius:12px;padding:.75rem;background:#fff} .infograph .kpi .eyebrow{letter-spacing:.06em;font-size:.72rem;text-transform:uppercase;color:#6a758a;margin-bottom:.25rem} .infograph .kpi strong{display:block;font-size:1.05rem} .infograph .kpi span{display:block;font-size:.9rem;color:#57627a} .ky-download a{text-decoration:none;border:1px solid var(–brand);padding:.5rem .85rem;border-radius:999px;color:var(–brand);display:inline-block;margin-right:.5rem} .ky-disclaimer{font-size:.9rem;color:#5b667a;background:#fbfbfd;border-top:1px solid #eef2f7;padding:1.25rem;margin-top:2rem}

Kentucky Mortgage Approval With No Credit Score

Simple steps for FHA, VA, USDA, and Conventional loans. If you have no credit score, you can still buy a home in Kentucky—here’s how.

Author: Joel Lobb, Senior Loan Officer — EVO Mortgage · NMLS #57916 · Company NMLS #1738461 · Louisville, KY

- Why this guide matters

- Quick Start: What to do first

- Program snapshot

- VA with no score

- FHA with no score

- Conventional with no score

- USDA with no score

- Non‑traditional credit examples

- Documents checklist

- FAQs

- References

- Get pre‑approved

Why this guide matters

You can buy a home in Kentucky even if you do not have a credit score. I help first‑time buyers with no scores every week. This site has deep, Kentucky‑specific guides on FHA, VA, USDA, and Conventional loans. That gives you simple steps, clear rules, and fewer surprises. This is our specialty, and we do it a lot.

See related guides: Kentucky FHA Loans · Kentucky VA Loans · USDA Rural Housing Kentucky · KHC Down Payment Assistance

Quick Start: What to do first

Step 1 — Pick the best program

- Use VA if you are eligible ($0 down for most with entitlement).

- Use USDA if the home is in an eligible rural area ($0 down).

- Use FHA for flexible credit rules and manual underwriting.

- Use Conventional when AUS approves (often with a co‑borrower who has a score).

Step 2 — Prove your payment history

Gather 12 months of on‑time payments for rent and 2–3 other bills (utilities, phone, insurance, daycare). Bank statements, invoices, or letters from the company work.

Program snapshot (side‑by‑side)

| Program | Purchases vs. Refis | Approval method | DTI rules | Tradelines & Rent | Notes |

|---|---|---|---|---|---|

| VA | Purchases only when no score is involved | Manual underwriting allowed up to 50% DTI with residual income. If DTI > 41%, meet 120% of VA residual income. | Up to 50% with strong residual income | 3 non‑traditional tradelines with 12 months on‑time history. Rent‑free letter if living rent‑free. | $0 down with entitlement; no formal loan cap with full entitlement (investor overlays may apply). |

| FHA | Purchases only when a borrower has no score | Even if AUS is Approve/Eligible, downgrade to manual when any borrower has no score. | All no‑score: 31/43. If one borrower has ≥580 and the other no score: up to 40/50 with compensating factors. | 3 non‑traditional tradelines per no‑score borrower; rent‑free letter if applicable. | HUD REO $100 down, escrow holdbacks, 203(h) disaster, Condo Single‑Unit Approvals allowed. |

| Conventional (Fannie Mae / Freddie Mac) | Purchases and refis as AUS permits | No‑score co‑borrowers allowed with DU/LPA Approve/Accept. Run both and follow the stronger findings. | Per AUS | If scored borrower provides >50% of income: no extra NTCs. If no‑score borrower provides >50%: 2 NTCs + 12‑month rent. | Pricing may be based on the scored co‑borrower’s profile when paired with a no‑score borrower. |

| USDA | Purchases | Run GUS. Enter 100 as the credit score for a no‑score borrower. | Typical ratios 29/41 unless GUS allows otherwise | If 12‑month rent is verified: add 1 extra NTC. If no rent: provide 3 NTCs. | $0 down for eligible rural properties (confirm property & income eligibility). |

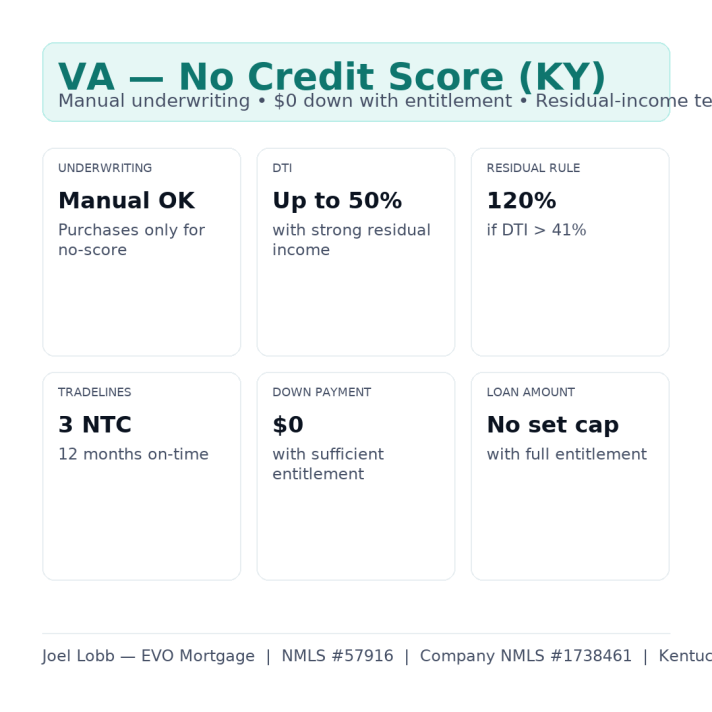

VA with no score

What to expect

- Manual underwriting allowed up to 50% DTI with strong residual income.

- 3 non‑traditional tradelines with 12 month on‑time history for any no‑score borrower.

- Rent‑free letter if you live rent‑free.

- $0 down available for eligible Veterans with entitlement.

Helpful link: VA Home Loan Program

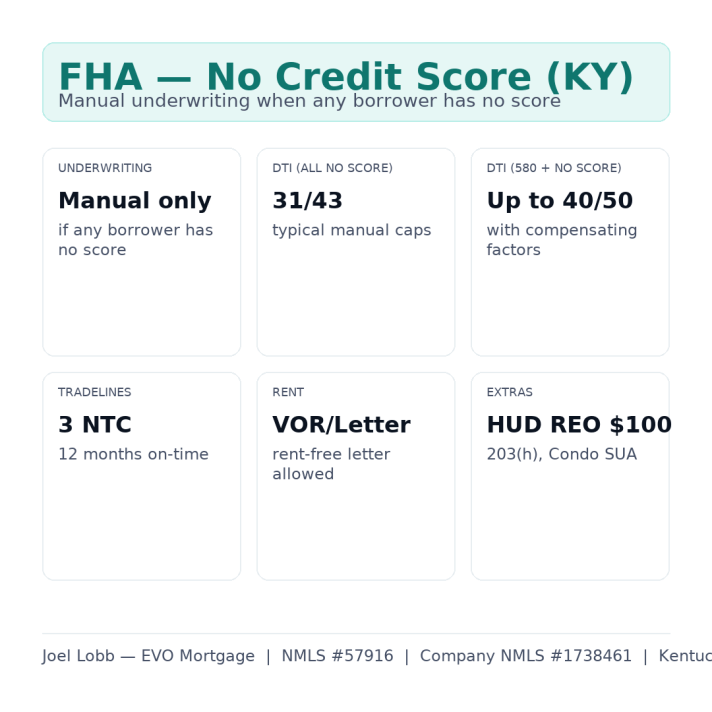

FHA with no score

What to expect

- Manual underwriting when any borrower has no score (even if AUS says Approve/Eligible).

- DTI caps: 31/43 when all borrowers have no score; up to ~40/50 with a 580+ co‑borrower and compensating factors.

- Three non‑traditional tradelines with 12 months of on‑time payments for each no‑score borrower.

- Rent verification for 12 months or a rent‑free letter, as applicable.

- Special allowances: HUD REO $100 down, escrow holdbacks, 203(h) disaster relief, Condo Single‑Unit Approvals.

Helpful link: FHA for Homebuyers

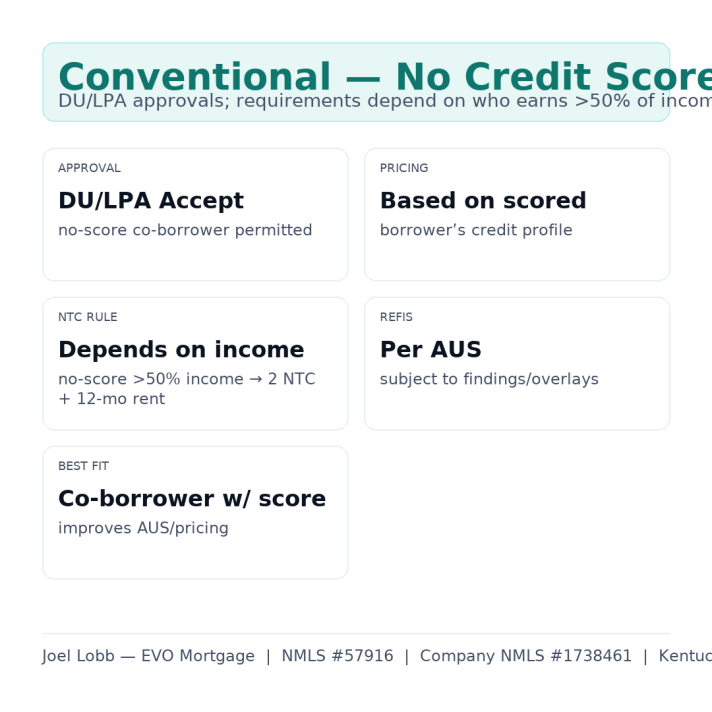

Conventional with no score

What to expect

- Run DU (Fannie) and LPA (Freddie). If you receive Approve/Accept, a no‑score co‑borrower is allowed.

- Pricing may be based on the scored borrower’s credit when paired with a no‑score co‑borrower.

- If the scored borrower provides more than 50% of qualifying income: no extra NTCs needed. If the no‑score borrower provides more than 50%: provide 2 NTCs + 12‑month rent verification.

Helpful links: Fannie Mae Single‑Family · Freddie Mac Single‑Family

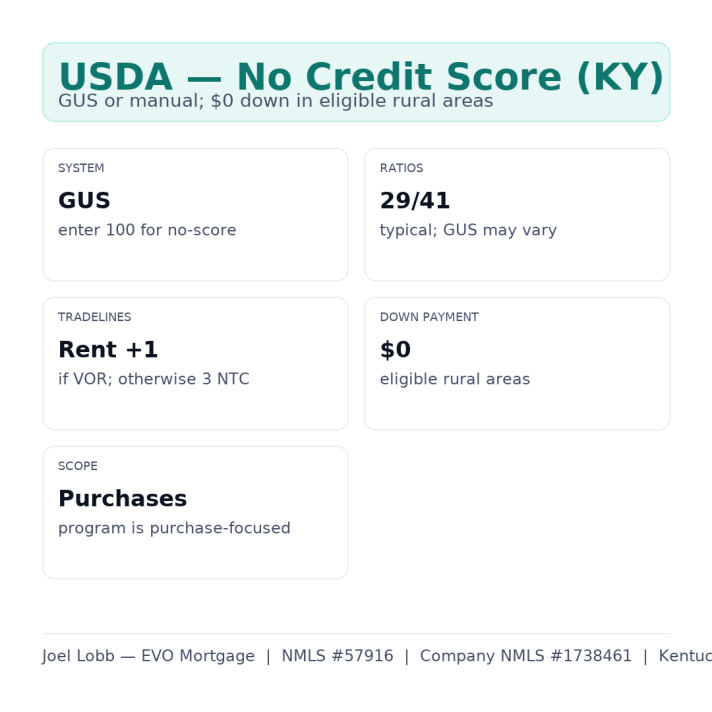

USDA with no score

What to expect

- We run GUS. For a borrower with no score, we enter 100 as the score value in the system.

- Typical USDA ratios are 29/41, but GUS may allow exceptions.

- If 12‑month rent is verified: provide rent + 1 extra non‑traditional tradeline. If no rent: provide 3 non‑traditional tradelines.

- $0 down for eligible rural properties. Check your address on the USDA map.

Helpful link: USDA Eligibility

Non‑traditional credit examples

- Rent or mortgage (VOR)

- Utilities: electric, water, gas

- Phone or internet

- Auto or renters insurance

- Daycare or tuition

- Streaming or subscription bills

- Medical payment plans

- Gym membership with monthly billing

Tip: we need 12 straight months of on‑time payments and a way to verify them.

Documents checklist

Identity & income

- Driver’s license and Social Security number

- 30 days of pay stubs and last 2 years W‑2s

- Last 2 months of bank statements

- Proof of other income (if any)

Non‑traditional credit

- 12‑month rent verification or rent‑free letter

- 2–3 other bills with 12 months of on‑time payments

- Invoices or letters from each company

- Matching bank statements when possible

FAQs: No Credit Score Mortgage Approval in Kentucky

Can I buy a house in Kentucky with no credit score?

Yes. VA, FHA, and USDA allow no‑score borrowers on purchases with manual underwriting and documented non‑traditional credit. Conventional loans may also work when AUS or manual underwriting requirements are met, often with a co‑borrower who has a score.

FHA: What are the DTI limits if I have no score?

When all borrowers have no score, FHA loans are manually underwritten with typical caps around 31/43. If one borrower has a 580+ score and you show strong compensating factors (like extra reserves or lower payment shock), ratios can stretch to about 40/50 under HUD rules.

FHA: What non‑traditional credit do I need?

Plan on three non‑traditional tradelines (rent, utilities, phone/Internet, insurance, daycare, subscriptions), each with 12 months of on‑time payments. If you live rent‑free, we’ll use a rent‑free letter instead of a rent history.

VA: Can I be approved with no score? What about residual income?

Yes. VA allows manual underwriting. If your DTI is over 41%, your household must meet at least 120% of the VA residual‑income benchmark based on your family size and region.

VA: Do I need a down payment or is there a loan cap?

Most eligible Veterans can buy with $0 down if they have full entitlement. VA does not set a formal loan cap with full entitlement, but investor and lender limits can still apply.

USDA: How does USDA handle no‑score files?

USDA uses GUS or manual underwriting. Without a score, we document non‑traditional credit per HB‑1‑3555 Chapter 10 and follow program ratios (commonly 29/41 unless GUS permits otherwise).

USDA: Do I need 12 months of rent history?

If you have rent, we verify 12 months and add at least one more non‑traditional tradeline. If you do not have rent history, we gather three non‑traditional tradelines.

Conventional (Fannie Mae): Can I qualify if my co‑borrower has a score?

Often yes. Fannie Mae permits loans when one or more borrowers lack a score if a non‑traditional credit history is documented and other Selling Guide rules are met. DU generally needs at least one borrower with a score; if none have scores, manual underwriting applies.

Conventional (Freddie Mac): What if I have no usable score?

Freddie Mac allows certain LPA Accept loans when not all borrowers have a usable score, and provides a path for borrowers without credit scores under specific conditions (fixed‑rate only; LTV/TLTV/HTLTV generally up to 95%, among other limits).

What should I avoid right before I apply?

Do not open new credit, take on buy‑now‑pay‑later plans, or make large undocumented deposits. Keep paying every bill on time and talk to me before changing jobs or moving money.

References (official program sources)

- FHA Single Family Housing Policy Handbook 4000.1 — HUD official handbook (updated Aug 13, 2025). HUD 4000.1

- VA Lenders Handbook, Chapter 4 — Credit Underwriting and residual income requirements. VA Chapter 4 PDF

- USDA Single Family Housing Guaranteed Loan Program, HB‑1‑3555 (Consolidated) and Chapter 10 — Credit Analysis & non‑traditional credit. USDA HB‑1‑3555 · Chapter 10 PDF

- Fannie Mae Selling Guide — B3‑5.4‑01 Eligibility for Loans with Nontraditional Credit; B3‑5.4‑03 Documentation & Assessment; B3‑5.1‑01 General Requirements for Credit Scores. B3‑5.4‑01 · B3‑5.4‑03 · B3‑5.1‑01

- Freddie Mac — Mortgages for Borrowers Without Credit Scores (Seller/Servicer Guide reference). Freddie Mac guidance PDF

Ready to get pre‑approved?

We specialize in no‑score mortgage approvals in Kentucky across FHA, VA, USDA, and Conventional. I will map your plan, list the exact documents you need, and show you the payment range you can expect.

Equal Housing Lender. EVO Mortgage Company NMLS #1738461 | Joel Lobb NMLS #57916. Not a commitment to lend. All loans subject to credit approval, property approval, program availability, and change without notice. AUS findings and agency handbooks (HUD/FHA, VA, USDA, Fannie Mae, Freddie Mac) – as well as investor overlays – control. Some features (such as no‑score refinances) may be unavailable. Always verify property eligibility and income limits for USDA and KHC programs.

{kind=link}

{kind=link}

{kind=link}

{kind=link}