Serving Louisville, Lexington, Bowling Green, Owensboro, Paducah & all 120 Kentucky counties

Kentucky Mortgage Broker for FHA, VA, USDA Rural Housing, KHC Down Payment Assistance & Conventional Loans

I’m Joel Lobb (NMLS #57916), a lifelong Kentucky resident with 20+ years in lending, and I’ve helped over 1,300 Kentucky families buy or refinance their homes.

My approach is straightforward: honest guidance, responsive service, and a clean path to closing.

Free, no-pressure guidance. Quick pre-approvals often within 6 hours. Typical closings 15–30 /apply/days (timeline depends on underwriting, appraisal, title, and program requirements).

Why Kentucky Borrowers Choose a Mortgage Broker Over a Big Bank

If you’ve ever felt like a “file number” at a large bank, you’re not alone. Many mega-banks only offer their in-house loan products. That can be fine when a borrower fits perfectly inside their boxes.

But in real life, Kentucky borrowers often have unique situations: variable income, overtime, self-employed income, VA eligibility, rural properties, KHC down payment assistance needs, or credit rebuilding after life events.

As an independent mortgage broker, I can shop your loan through a network of mortgage lenders to identify competitive rate options and program solutions that may not be available at a single bank.

In practical terms, that means more flexibility and a better chance of matching your goals with the right underwriting lane.

- Access to multiple lender options instead of “one bank, one deal.”

- Program-fit strategy for FHA, VA, USDA Rural Housing, KHC, and Conventional.

- Direct, responsive communication and fewer last-minute surprises.

- Clear guidance on credit, income, assets, and documentation from day one.

Bottom line: my job is not to “sell” you a loan. My job is to structure the right mortgage plan and help you close on time with confidence.

Serving All 120 Kentucky Counties

Kentucky is diverse — from Louisville and Lexington to small towns and rural communities statewide. I proudly serve borrowers in every region of the Commonwealth, including:

Jefferson County, Fayette County, Warren County, Kenton County, Boone County, Campbell County, Hardin County, Bullitt County, Oldham County, Christian County, McCracken County, Daviess County, and all 120 counties in Kentucky.

If you’re purchasing in Kentucky, refinancing in Kentucky, or relocating to Kentucky, you can call or text me directly at 502-905-3708.

Kentucky Home Loan Programs I Offer

FHA Loans in Kentucky

FHA loans are popular for first-time buyers and borrowers who need flexible credit guidelines and low down payment options. FHA financing may be a strong fit if you’re rebuilding credit,

have limited savings, or need a program designed for accessibility.

Learn more on my FHA page: Kentucky FHA Loans.

VA Loans in Kentucky

VA loans are a powerful benefit for eligible Veterans, active-duty service members, and certain surviving spouses. VA financing can offer strong terms, including potential zero down options and competitive pricing.

If you’re moving to Kentucky from another state or buying your first home using VA, I’ll guide you through eligibility, documentation, and a smooth closing plan.

Learn more here: Kentucky VA Home Loans.

USDA Rural Housing Loans (100% Financing Eligible Areas)

USDA Rural Housing loans can provide 100% financing for eligible properties and borrowers — making it one of the strongest no-down-payment options in Kentucky.

Many borrowers are surprised how many areas qualify, even near larger cities.

Get details here: Kentucky USDA Rural Housing Loans.

KHC Down Payment Assistance Programs

Kentucky Housing Corporation (KHC) programs can help qualified buyers who need down payment assistance. These options can be especially helpful for first-time homebuyers who have stable income

but need help bridging the cash-to-close gap.

Learn more here: KHC Down Payment Assistance.

Fannie Mae Conventional Loans

Conventional financing through Fannie Mae can be an excellent fit for borrowers with stronger credit profiles, stable income, and long-term homeownership goals.

It can also be the right option for certain refinances depending on the situation.

Learn more: Kentucky Conventional Loans.

What Makes My Process Different

A mortgage is not just an interest rate. It’s underwriting strategy, documentation, timeline management, communication, and problem-solving.

My process is designed to reduce stress and increase certainty.

Fast, clear pre-approvals

I move quickly, but I do not cut corners. You’ll get a plan built on documentation and realistic underwriting expectations.

Direct access to me

You can call or text me directly. No call centers. No getting passed from person to person.

Transparency from day one

If there’s a problem, you’ll know early. If something is borderline, we address it up front.

Closing execution

The goal is a predictable closing timeline with strong communication between you, your agent, title, and underwriting.

Free, Honest Second Opinions Are Welcome

If you already have a loan estimate from a bank or another lender, I’m happy to compare it and explain what it means in plain English.

Many borrowers don’t realize how rate, points, lender fees, mortgage insurance, and program fit impact the real cost of the loan.

If you want a straight answer, you’ll get one. If your current quote is strong, I’ll tell you that too. My goal is for you to make a confident decision.

Ready for a Kentucky Mortgage Pre-Approval?

Call or text me directly at 502-905-3708, or start your free pre-approval online.

You will receive honest, up-front guidance with a clear next-step plan.

Common Questions Kentucky Homebuyers Ask

How fast can I get pre-approved?

In many cases, I can turn around a pre-approval within 6 hours once I have the core documentation needed.

Timing can vary depending on complexity, income type, and documentation.

How long does it take to close a mortgage in Kentucky?

Many purchases close in 15–30 days, but timelines depend on the appraisal, title work, underwriting conditions, and program requirements.

My process focuses on minimizing delays through accurate upfront planning and fast communication.

Do you offer no-down-payment options?

Yes. VA loans and USDA Rural Housing loans may offer eligible borrowers a path to 0% down.

Eligibility depends on program guidelines, income, credit, and (for USDA) property location.

Can you help if I was denied by a bank?

Often, yes. A denial is not always the end — it may be a program-fit issue, documentation issue, or lender guideline mismatch.

I’ll review the situation and give you a clear plan for next steps, even if that means improving credit, adjusting the structure, or selecting a different program.

Reblogged this on Louisville Kentucky Mortgage Loans and commented:

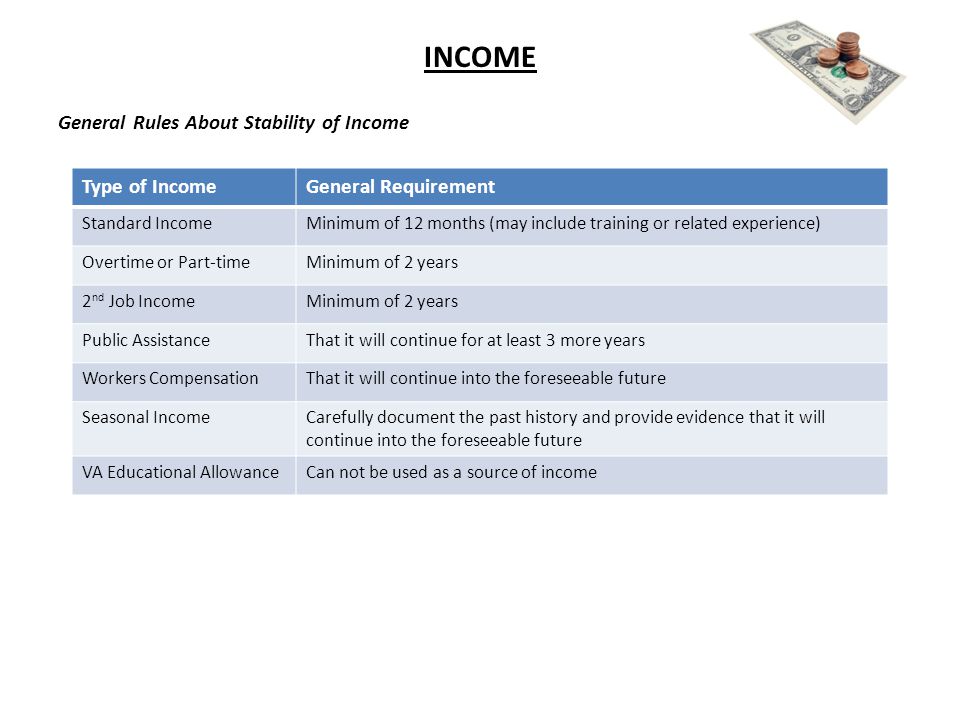

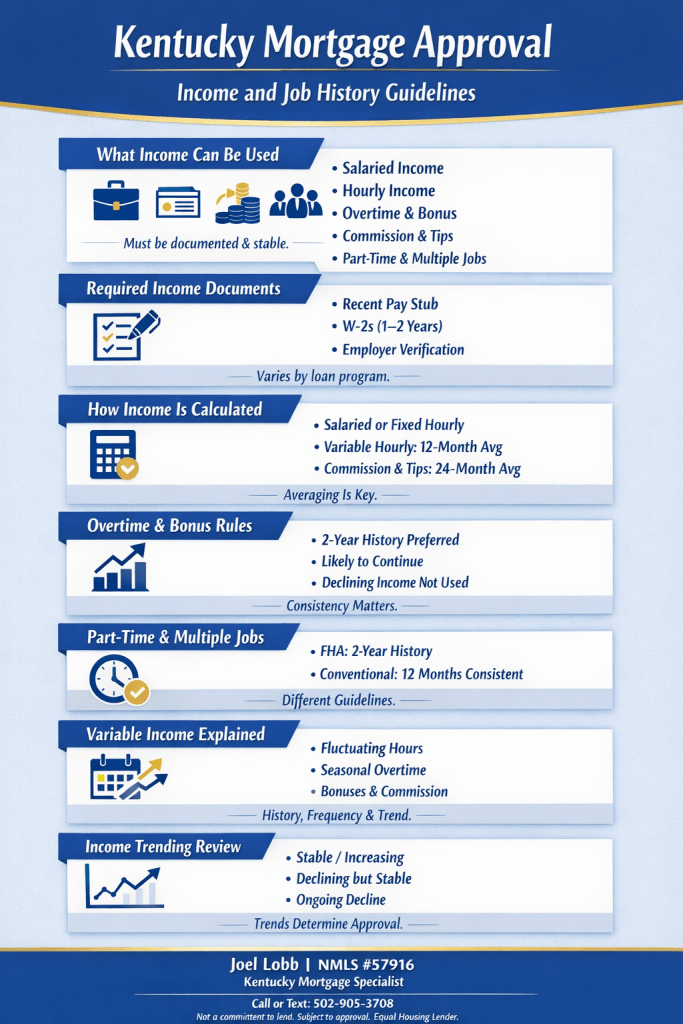

What kind of income is allowed and needed for a FHA, VA, USDA and Fannie Mae Mortgage Loan Approval in Kentucky?

LikeLike