Author: Kentucky Mortgage Broker Offering FHA, VA, USDA, Conventional, and KHC Down Payment Assistance Home Loans

Thank you for visiting. I hope you find this website both informative and empowering as you explore your mortgage options. My goal is to help you feel confident in selecting the right home loan for your unique situation. I proudly serve all 120 counties in Kentucky, offering a full range of mortgage loan programs, including: FHA Loans VA Loans USDA Rural Housing Loans Fannie Mae Conventional Loans KHC Down Payment Assistance Programs With over 20 years of lending experience, I’ve had the privilege of helping more than 1,300 Kentucky families achieve their homeownership goals. Whether you're a first-time homebuyer or seeking a second opinion, I’m here to offer honest, no-pressure advice—always free of charge. I am dedicated to: Attending as many closings as possible Providing responsive, personalized service Ensuring quick, efficient, and accurate loan processing Making myself accessible every step of the way I've been consistently recognized as a top mortgage loan officer in Kentucky for VA, FHA, USDA, and KHC programs. I take pride in being thorough, transparent, and attentive with each and every client. Please take a moment to read my reviews below. If you have questions or need guidance, feel free to call or text me directly. Call/text at 502-905-3708. Free Mortgage Pre-Qualifications same day on most applications.

Email me at kentuckyloan@gmail.com with your questions

I specialize in Kentucky FHA, VA ,USDA, KHC, Conventional and Jumbo mortgage loans. I am based out of Louisville Kentucky. For the first time buyer, we offer Kentucky Housing or KHC loans with down payment assistance.

This website is not an government agency, and does

not officially represent the HUD, VA, USDA or FHA or any other government agency.

NMLS# 57916 http://www.nmlsconsumeraccess.org/

Joel Lobb Senior Loan Officer/p>

call/text phone: (502) 905-3708 kentuckyloan@gmail.com Company ID #1738461

EQUAL HOUSING LENDER

http://www.mylouisvillekentuckymortgage.com/

FAQ’s about Kentucky FHA Home Loans

FHA

FHA 203k Loan/Rehab

fha approved condo

FHA extends “Anti-Flipping Waiver”

FHA Loans

FHA Loans Kentucky Housing First time home buyer

FHA Mortgage Guide

FHA property requirements

fico credit score

fico credit scores

First time home buyer

First Time Home Buyer Loans–Kentucky

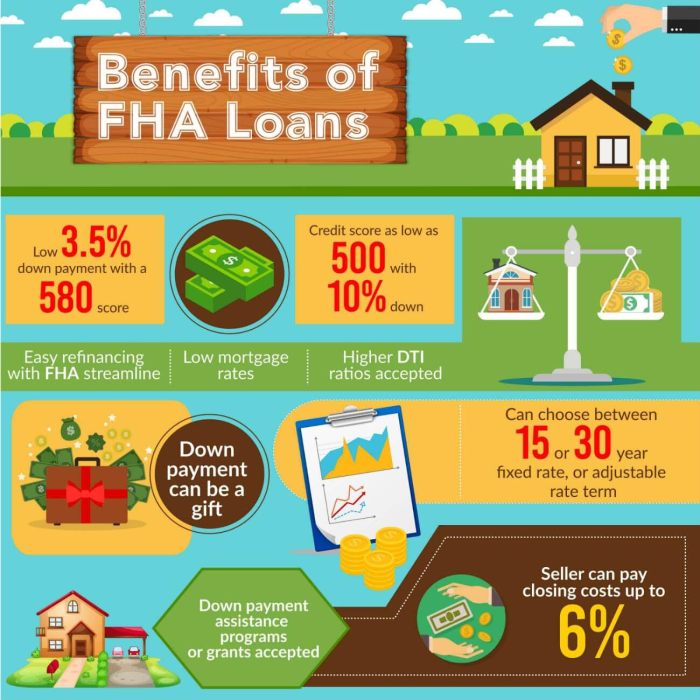

Kentucky FHA loans allow buyers with down payments as little as 3.5% to buy a home, and with many state-sponsored down payment assistance programs like KHC or Kentucky Housing Agency down payment asssitance program of up to $6000 currently to use for your own down payment, Kentuck borrowers using FHA loans can can get the loan with zero money down.

They’re are other down payment assistance programs in KEntucky see below:

FHA’s New Student Loan Rule Could Impact Kentucky Mortgage Borrowers

Student Loan Payment Calculations for FHA, VA, USDA, and Fannie Mae Loans in Kentucky

Fannie Mae Guidelines for Student Loans

If a monthly payment is on the credit report, the lender may use that amount for qualifying purposes.

If a monthly payment is on the credit report is incorrect, the lender may use the monthly payment on the most recent student loan statement

If the monthly payment on the credit report is zero, the lender must use one of the following options to calculate the payment for qualifying purposes

Document the borrower is on an income driven payment plan and the actual monthly payment is zero

Use 1% of the outstanding student loan balance as the monthly payment

Calculate a fully amortized payment using documented loan repayment terms

FHA Guidelines for Student Loans

Regardless of the payment status (currently in payment or deferred), the lender must use either:

The greater of:

1% of the outstanding balance; or

The monthly payment reported on the credit; or

Calculate a fully amortized payment using documented loan repayment terms

USDA Rural Housing Guidelines for Student Loans

Regardless of the payment amount reporting on the credit, the lender must include the payment as follows:

A permanent amortized, fixed payment may be used in the debt ratio when the lender retains documentation to verify the payment is fixed, the interest rate is fixed, and the repayment term is fixed.

Payments for deferred loans, Income Based Repayment (IBR), Graduated, Adjustable, and other types of repayment agreements which are not fixed cannot be used in the total debt ratio calculation. One percent of the loan balance reflected on the credit report must be used as the monthly payment. No additional documentation is required.

VA Mortgage Guidelines for Student Loans

If the borrower can document the student loan will be deferred 12 months from the closing date, the monthly payment does not need to be considered

If a student loan is in repayment or scheduled to begin repayment within 12 months from the closing date, the threshold payment amount must be calculated by using 5% of the loan balance divided by 12 months

If the payment reporting on the credit report is greater than the threshold payment calculation amount, then the credit report payment must be used for ratios.

If the payment reporting on the credit report is less than the threshold payment calculation and the lender is using the lower payment to qualify the borrower then:

A statement from the student loan servicer reflecting the actual loan terms and payment information must be included in the file.

The statement must be dated within 60 days of closing

It is the underwriter’s discretion to use the lower payment

Just last month, the Federal Housing Authority instituted new rules for how FHA mortgage lenders should calculate student loan debt. FHA loans, which are the preferred type of mortgage for first-time buyers, are backed by the federal government and require lower down payments than conventional mortgages. The credit requirements for FHA loans are also much more lenient

But some of that leniency, at least when it comes to student loan debt, changed on September 14, when the FHA tightened its requirements for how mortgage lenders treat deferred student loan debt. In the past, student loan debt that was deferred for more than 12 months before the mortgage closing date wasn’t counted in the debt-to-income ratio. Now, 2% of that debt is included in the calculation…

What is Kentucky USDA Rural Development Guarantee?

Kentucky USDA Rural Development Guarantee USDA loans offer 100% financing options on home purchases in rural areas of Kentucky. Properties though can be located within city limits and in subdivisions depending on population density of that particular County of Kentucky. Jefferson and Fayette Counties, the two largest counties of Kentucky are not eligible for Rural Development Loans.

The Kentucky Rural Development loan program is primarily used to help low to moderate income individuals or households to purchase homes and the applicants need to be within 115% of the median income for the area. Most counties will allow up to $82,700 for a family of four and up to $109,200 for a family of five or more for household incomes to be eligible for RHS loans.

Some areas of Northern Kentucky you can make more than that: see below

Congress Passes VA Loan Bill for Kentucky VA Home Buyes

The President is expected to sign H.R. 299, the ‘Blue Water Navy Vietnam Veterans Act.’ This legislation includes language which will eliminate the cap on the VA home loan guarantee.

The President is expected to sign H.R. 299, the ‘Blue Water Navy Vietnam Veterans Act.’ This legislation includes language which will eliminate the cap on the VA home loan guarantee.

How to qualify for a Kentucky FHA Home Loan ?

How to qualify for a Kentucky FHA Home Loan ?