00% Financing Zero Down

2-1 and 1-0 buydowns for Kentucky Rural Housing USDA RD loans Interest Rates.

2-1 and 1-0 buydowns for Kentucky Rural Housing USDA RD loans Interest Rates.

2022 Kentucky USDA Income and Property Guidelines

2022 Kentucky USDA Income Limits Increased

2022 Kentucky USDA Mortgage Guides Updated

2023 Kentucky USDA Underwriting Guideline Mortgage Changes for Income, Credit, Work History and Assets

40 year term loan

502 Guaranteed Loan

620 credit score USDA Loan Kentucky

annual mi fee

Appraisals

bank statements

Bankruptcy

Bullitt County KY

cashout refinance

collections on USDA loans

conditional commitments

Conventional Mortgage Rates Today

coronavirus Kentucky USDA Loans

COVID-19 Kentucky USDA Rural Housing Loan

Credit Bad

credit reports

credit scores

Credit Waiver

Current USDA and RHS Guidelines

Debt Ratio and Deferred Student Loans

debt ratios

Direct Loan USDA

DIRECT LOANS

Down Payment and Closing Costs Assistance

down payment grant

down payment grant ky housing

employment

fico scores

Foreclosures

funds available for 2021 USDA loans

Guarantee Fee and the Annual Fee for RHS loans

Guaranteed Section 502 Loans

GUS Accept Findings USDA

Home Insurance Maximum Deductible

Homes for Sale (Foreclosures owned by USDA/RHS KY

Homes for Sale in Kentucky by USDA

Income Based Repayment (IBR) plans

INCOME ELIGIBILITY

Income Limits

ineligible areas

Interest Rate Buydowns

job gaps

job time

Kentucky Direct Single Family Housing Program

Kentucky FHA

kentucky first time home buyer

KHC

low-interest loans from the U.S. Department of Agriculture

manufactured homes

map changes for 2013 Ky USDA homes

MAPS

MI Changes for USDA Oct 2011

mobile homes

mortgage insurance annual fee

Payment Shock

PAYOFFS

POA Power of Attorney USDA Loans

property eligibility

Property Eligibility Cities

Property Eligilibity

Property/Appraisal Requirements for USDA Loan

Rates Today

Refinance Pilot Program Streamline

refinance USDA loan

rent

rural development

Rural Development loan

Section 504 Repair Loan and Grant Program

Self-employed USDA Loans

Seller Concessions

seller paid closing costs

septic test

SFH Direct property

short sale USDA loans

Student Loans

Subsidy Recapture

Swimming Pools for USDA Loans

tradeline minimum for USDA Approval

tradelines on USDA lanos

turn times underwriting

Uncategorized

underwriting turn times files USDA

USDA

USDA /Rural Housing Loan Offices in Ky

USDA Loan

USDA REVISIONS TO HB-1-3555

USDA RURAL DEVELOPMENT DIRECT HOUSING LOANS

USDA/RHS Income limits by Ky Counties

VA

well test

work history

Zero Down Home Loans

Kentucky Rural Housing USDA Buydown Program

Kentucky USDA Underwriting Guideline Mortgage Changes for Income, Credit, Work History and Assets

Kentucky USDA Underwriting Guideline Mortgage Changes for Income, Credit, Work History and Assets

What credit score do you need for a Kentucky mortgage loan approval in 2022?

$0 Down, 100% Financing for Kentucky USDA Rural Housing Loans

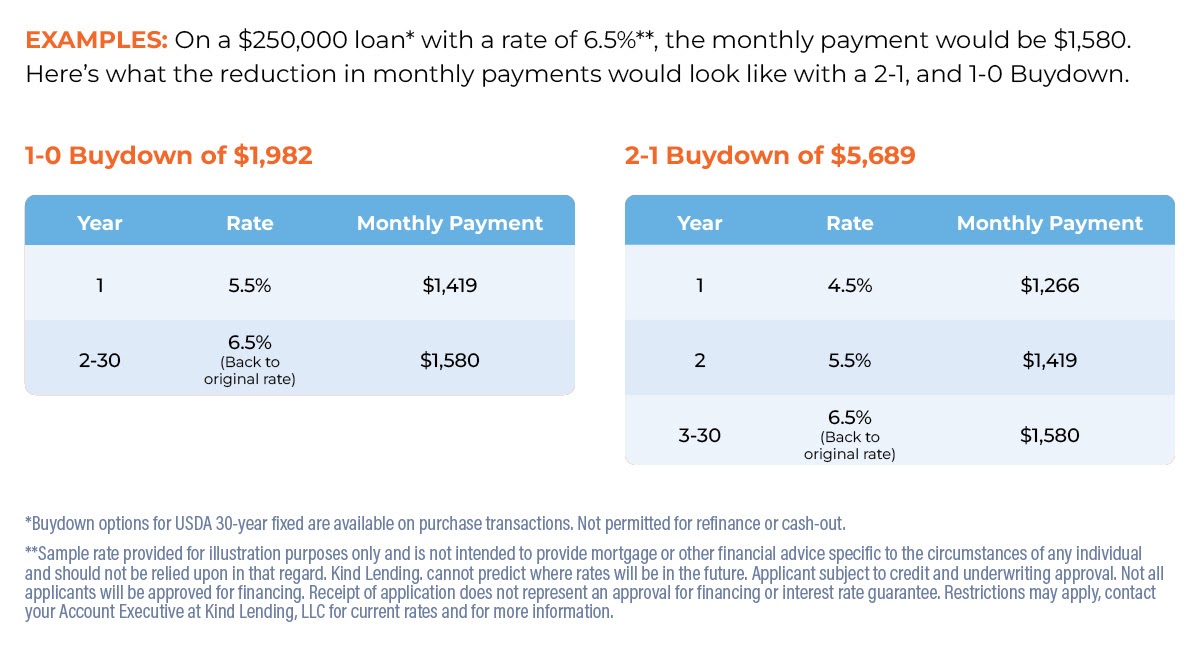

The Kentucky Rural Housing USDA Buydown Program provides simple financing options that lowers the interest rate on a mortgage for either 1 year (1-0) or 2 years (2-1), before it rises to the regular permanent rate. Specifics2-1, and 1-0 temporary interest rate buydowns are allowed on 30 year fixed-rate mortgages for principal residences, purchase only. Not permitted on refinance transactions.The seller or agent may provide funds for the temporary interest rate buydown, subject to standard interested party contribution limits. Lender paid buydowns are not offered. The borrower is qualified at the note rate fully amortized (not the buydown rate)Minimum credit score for loans with buydown is 620

2-1 and 1-0 buydowns for Kentucky Rural Housing USDA RD loans Interest Rates.

What are Buydowns for Kentucky USDA RD Loans?

The Kentucky Rural Housing USDA Buydown Program provides simple financing options that lowers the interest rate on a mortgage for either 1 year (1-0) or 2 years (2-1), before it rises to the regular permanent rate. Specifics2-1, and 1-0 temporary interest rate buydowns are allowed on 30 year fixed-rate mortgages for principal residences, purchase only. Not permitted on refinance transactions.The seller or agent may provide funds for the temporary interest rate buydown, subject to standard interested party contribution limits.Lender paid buydowns are not offered.The borrower is qualified at the note rate fully amortized (not the buydown rate)Minimum credit score for loans with buydown is 620

Have Questions or Need Expert Advice? Text, email, or call me below:

Joel Lobb Mortgage Loan Officer Individual NMLS ID #57916

Rural Development Kentucky Underwriting Guideline Mortgage Changes for Income, Credit, Work History and Assets

Chapter 9 – Income Analysis

Paragraph 9.3 is being revised as follows: o To clarify that lenders must verify the income of each adult household member for the previous 2 years, which is consistent with the requirements in 7 CFR 3555. o To clarify under “full income documentation”, the lender must obtain W-2s or IRS Wage and Income transcripts, in addition to paystubs. o To change the term “streamlined documentation” to “alternative income documentation” to remove confusion with the streamlined refinance product. o To clarify under “self-employed income documentation” that if ownership interest is less than 25%, neither the “Business Owner” or “Self-Employed” options should be selected in GUS. o To clarify the Verbal Verification of Employment must be obtained within 10 business days of loan closing and confirmation a self-employment business remains operational must be…