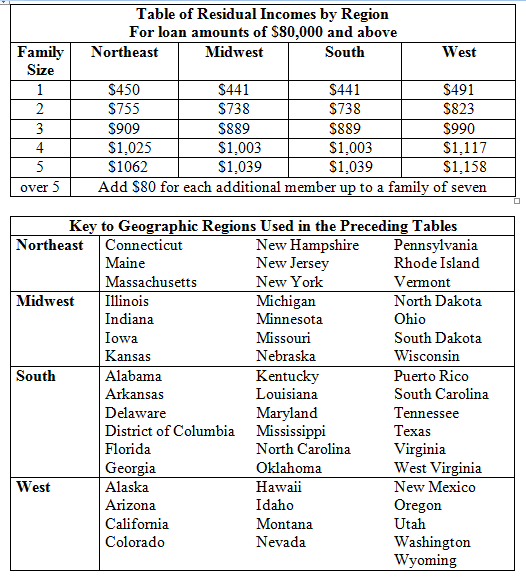

▪ Calculate the total gross monthly income of all occupying borrowers ▪ Deduct from gross monthly income the following items: ▫ State income taxes ▫ Proposed total monthly fixed payment (i.e. PITIA + MIP) ▫ Federal income taxes ▫ Estimated maintenance and utilities ▫ Municipal or other income taxes ▫ Job related expenses (e.g. childcare) ▫ Retirement or Social Security ▫ Gross upp of any Non-Taxable Income ▪ Subtract the sum of the deductions from the table above from the total gross monthly income of all members of the household of the occupying borrowers ▪ The balance is residual income Calculating Gross Monthly Income: ▪ Gross monthly income should be calculated only for the occupying borrowers consistent with the requirements of HUD Handbook. ▪ Do not include bonus, part-time or seasonal income that does not meet the requirements for effective income as stated in HUD Handbook. ▪…

Minimal credit score requirements – NO minimum score

Low monthly mortgage insurance

Home must be located in an eligible area

Home must meet property eligibility requirements

Fill out worksheet to get additional information about qualifying

Must be a regular stick-built home

Single Close Construction Program available

USDA to USDA Streamline Refinances available

SFH Direct Loan and Grant Programs

February 7, 2022

Fee Increases for Origination Appraisals and Conditional Commitments

An Unnumbered Letter (UL) dated February 4, 2022, has been issued which increases the appraisal fee to $750 and the conditional commitment fee to $825 under the direct programs. The fee increases are effective March 6, 2022. The increased fees reflect market price increases for origination appraisals in rural areas and the average cost of appraisals under the programs’ nationwide contract with the Appraisal Management Companies.

As with all loan programs, the USDA Loan requires that an independent appraiser inspect the subject property in order to determine the property value. Specific to a USDA Loan, the appraisal report will be conducted by an FHA approved appraiser. The appraisal report must include verbiage or similar verbiage:

“The subject meets minimum standards as set under guidelines established by the U.S. Department of Housing and Urban Development and indicated in Handbooks 4000.1”

No different from a FHA or VA appraisal inspection, the appraiser is required to document all property deficiencies that preclude the appraiser from signing off on their report. A property deficiency is any defect to the house that the appraiser deems necessary to have repaired to ensure compliance to the loan program guidelines. Typical examples of property deficiencies include: