How long will it take to close on your Rural Development USDA Loan in Kentucky?

On average, 30 to 45 days is usually okay. Sometimes quicker than 30 days, if the file is clean and submitted early to USDA office and the appraisal comes back okay.

It may take a 2-3 day longer turn time to Underwrite a USDA loan vs FHA, VA, Conventional loan. Not that big of a difference

The loan approval process for a USDA Loan is not like any other loan. Like all loan programs, the USDA Loan will have a lender that will assign the loan file to an Underwriter, who in turn will determine if the loan meets the loan program guidelines for approval.

Unlike other loan program, once the loan is approved by the lender/Underwriter, the file will be sent to one of the centralized processing sites for the Rural Development Offices in…

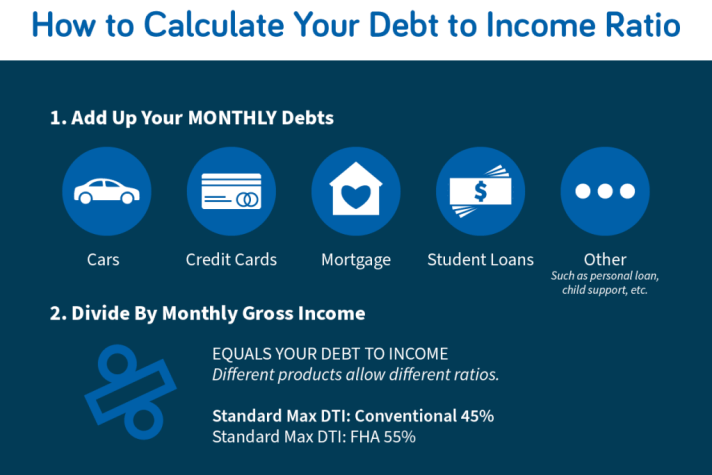

Your debt-to-income ratio, technically speaking, is all of your monthly debt payments divided by your gross monthly income—that is, the percentage of your gross monthly income that goes towards payments for rent, mortgage, credit cards, and other debt. This is how lenders measure your ability to manage the monthly mortgage payments to repay the money you’ll be borrowing.

To calculate your debt-to-income ratio, add up your monthly debts—this includes car payments, credit cards, mortgages, and student loans. Divide this amount by your monthly gross income, and you’ll get your DTI ratio.

For reference, the standard maximum DTI for conventional loans is 45%, and for FHA loans it’s 55%. Of course, the maximum DTI depends on the home loan.