USDA Loan assumes a very conservative perspective on financing homeowners who already own a home, unless the borrower can prove that the current home is not "adequate or suitable" for the borrower's needs.

Kentucky USDA Rural Development Loan Program:

Kentucky USDA Mortgage Lender for Rural Housing Loans

Kentucky USDA Mortgage Lender for Rural Housing Loans

The following is a list of the “nuts and bolts” of the Kentucky USDA Rural Development Loan Program:

- The house has to be located in a Kentucky USDA Rural Development Loan Program: area designated as an USDA eligible area.

- To determine the USDA approved designated areas, reference the following USDA map instructions:

- Go the USDA Rural Development Website

- On the top left hand side, click “Single Family Housing Guaranteed”

- Click “Accept”

- Enter the property address to determine if a specific house or general area is located in an USDA eligible area

- The household income must be moderate as determined by USDA. The USDA Loan evaluates household income, which includes the combined income of all adults living in the household; even if they are not on the mortgage loan. Click here to determine your household income eligibility.

- If it appears that the household income exceeds the moderate income thresholds established by USDA, do…

View original post 398 more words

Louisville Kentucky FHA Loans

Conventional loan

A conventional loan isn’t insured or guaranteed by a government entity. You can take one out through a private lender like a bank, credit union or mortgage company. While conventional loans are more difficult to qualify for than government loans, they’re also usually more flexible.Minimum credit score: 620

Minimum down payment: 3%

May be good for: Borrowers with good credit and minimal debt

Fannie Mae HomeReady

HomeReady is a conventional mortgage loan offered by Fannie Mae. If you apply for one, you can use income from your parents, grandparents, relatives and others to help you get approved. Upon approval, you may get rid of your private mortgage insurance, or PMI, after you pay down 20% of your home’s value.Minimum credit score: 620

Minimum down payment: 3%

May be good for: Borrowers with lower-than-average incomes

FHA loan

FHA loans are insured by the Federal Housing Administration. While these loans have low down payment and credit score requirements, you’ll be required to pay mortgage insurance to protect the lender in the event you default.Minimum credit score: 500

Minimum down payment: 3.5% if your credit score is 580 or higher; 10% if your score falls in the 500-579 range

May be good for: Borrowers with lower credit scores and down payment amounts

Freddie Mac Home Possible

The Freddie Mac Home Possible mortgage has a low down payment of 3%. But in order to qualify, you can’t earn more than 100% of the annual median income in your area.Minimum credit score: 660

Minimum down payment: 3%

May be good for: Borrowers with lower incomes and down payment amounts

Non-qualified (non-QM) mortgage

A non-qualified (non-QM) mortgage is for homebuyers who are unable to meet the strict criteria of a qualified mortgage, which meets federal guidelines. It can allow you to get approved for a home loan if you’re self-employed, work a nontraditional job or lack the documentation that most mortgages require.Minimum credit score: Varies by lender

Minimum down payment: Varies by lender

May be good for: Borrowers who are self-employed or earn alternative sources of income

USDA loan

Backed by the United States Department of Agriculture, a USDA loan is a low-interest, zero-down-payment mortgage that can help you finance a home in an eligible rural area.Minimum credit score: 640

Minimum down payment: 0%

May be good for: Borrowers with low to moderate incomes who want to buy a home in a rural area

VA loan

A VA loan is guaranteed by the United States Department of Veterans Affairs. As long as you’re an active service member, veteran or eligible spouse, you may get approved for a VA loan with 0% down and no PMI. But keep in mind that you’ll likely have to pay a funding fee of up to 3.6% of your loan amount.Minimum credit score: Varies by lender

Minimum down payment: 0%

May be good for: Borrowers who are active service members, veterans or eligible spouses

Louisville Kentucky Mortgage Loans

Conventional vs. FHA vs. VA loans in Kentucky

One of the big questions you’ll have to answer when you are ready to buy a home is what type of mortgage loan to choose. There are plenty of options out there, with conventional and FHA being among the most popular. Here’s what you need to know about these common mortgage choices.

Funding

Federal Housing Administration (FHA) loans are backed by that government agency with the intention of making mortgages more affordable to lower-income homebuyers. Those with less-than-ideal financial qualifications have found help from FHA loans.

Conventional loans are guaranteed by the government-sponsored entities Fannie Mae and Freddie Mac. These are not directly made or backed by the federal government, but once made by a private lender, Fannie or Freddie promise to buy them, taking the risk away from the lender and giving them more incentive to make more loans.

Down Payment

View original post 746 more words

Kentucky First-Time Home Buyer Loan Programs

Louisville Kentucky Mortgage Broker Offering FHA, VA, USDA, Conventional, and KHC Zero Down Payment Home Loans

Louisville Kentucky Mortgage Loans

KHC loan – Kentucky First-Time Homebuyer Loan Programs for FHA, VA, KHC and USDA Mortgage Loans in KY

Home Loans Preapproval Checklist

- A driver’s license or U.S. passport

- A Social Security number or card. If not a U.S. citizen, a copy of the front and back of your green card(s)

- Verification of employment

- Copy of their credit reports from the three national credit bureaus

- Recent pay stubs covering the last 30 days

- W-2 forms from the previous two years

- Proof of any additional income

- Last two years of personal federal income tax returns with all pages and schedules. If self-employed, last two years of individual federal income tax returns with all pages and schedules, as well as a business license, a year-to-date profit and loss statement (P&L), a balance sheet, and a signed CPA letter stating you are still in business

- Bank account statements proving that you have enough to…

View original post 688 more words

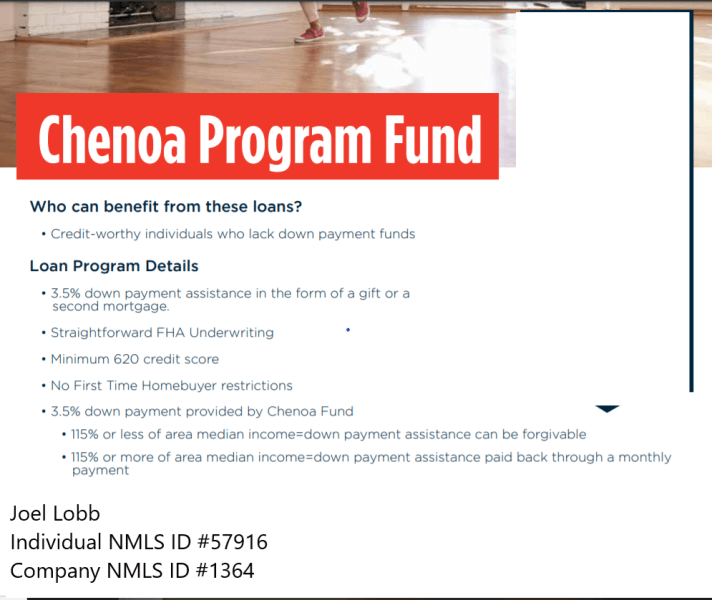

Chenoa Fund Down Payment Assistance Program in Kentucky

Chenoa Fund Down Payment Assistance Program in Kentucky

Louisville Kentucky Mortgage Loans

This Program is for any eligible potential home buyer and we operate in every state except for New York. In order to apply, you will need to work with an approved lender in your area. They will take and submit your application, assist to find the right program, and guide you through the process. The approved lender would assist with both the primary mortgage and the down payment loan and would be the one to provide any rate information.

In what state and county are you looking to purchase your home? We can send a list of approved lenders close to you that you can reach out to and apply.

You can find some general information about our program here: https://chenoafund.org/homebuyer/providing-down-payment-assistance-on-fha-and-conventional-loans.

In short, Chenoa Fund covers the entire down payment and provides 3.5% and 5% assistance on FHA and 3% and 5% on Fannie Mae conventional loans. Some basic information…

View original post 387 more words