Yesterday you may have read the blog post on questions to ask yourself before applying for a mortgage. Here are 5 additional that you may want to think about before you go into your meeting with your loan officer.

Here are questions 6-10 that you may need to get answers to before completing your application:

6. How Long Until We Can Close Our Loan?

Loan closing times are based on a number of factors. Closing dates may be delayed if there are missing documents or other underwriting delays. Speak with the loan officer to get an estimate on the time from application to closing.

7. What Possible Delays May I Face In Closing?

There are a number of delays that often cannot be avoided. However, some can be avoided by making sure you provide your loan officer with all the documents they request in a timely manner. In some cases…

New Condominium Approval Rule For Kentucky FHA Condo Mortgage Loans

The Federal Housing Administration (FHA) announced the publication of its Condominium Project Approval Final Rule effective with new case number assignments on or after October 15, 2019.

For more information, please read the press release issued by the Department of Housing and Urban Development (HUD).

Kentucky Mortgage loans done through FHA’s new condo rule and the new Condominium Project Approval section of the Single-Family Housing Policy Handbook were designed to be flexible and responsive to market conditions, and provide a comprehensive revision to Kentucky FHA condominium project approval policy. In particular, the new policy will allow certain individual condominium units to be eligible for

FHA Loan: “FHA loans are ideal for those who have less-than-perfect credit and may not be able to qualify for a conventional mortgage loan. The size of your required down payment for an FHA loan depends on the state of your credit score: If your credit score is between 500 and 579, you must put 10% down. If your credit score is 580 or above, you can put as little as 3.5% down (but you can put down more if you want to).”

Conventional Loan: “It’s possible to get approved for a conforming conventional loan with a credit score as low as 620, although some lenders may look for a score of 660 or better.”

USDA Loan: “While the USDA doesn’t have a set credit score requirement, most lenders offering USDA-guaranteed mortgages require a score of at least 640.”

VA Loan: “As with income levels, lenders set their own minimum credit requirements for VA loan borrowers. Lenders are likely to check credit scores as part of their screening process, and most will set a minimum score, or cutoff, that loan applicants must exceed to be considered.”

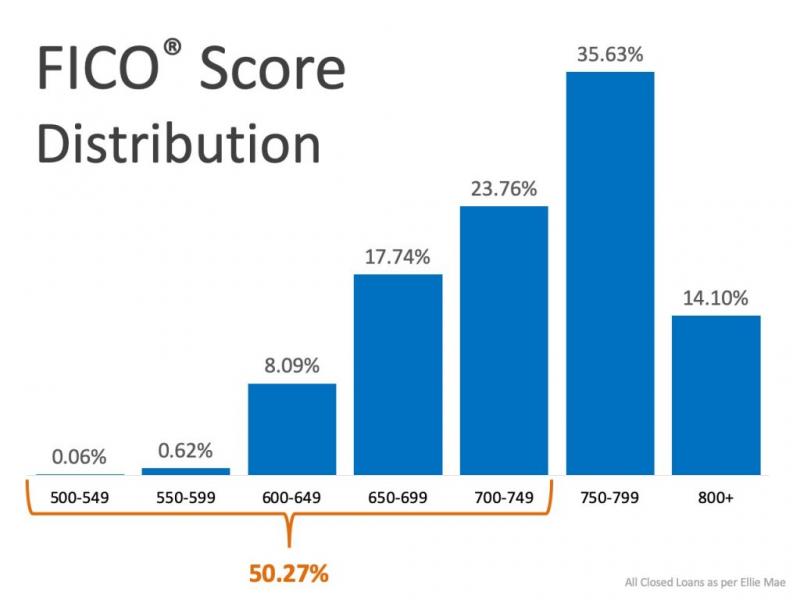

It’s common knowledge that your FICO ® score plays an important role in the homebuying process. However, many buyers have misconceptions regarding what exactly is required to get the loans they need. While a recent announcement from CNBC…

It’s common knowledge that your FICO® score plays an important role in the homebuying process. However, many buyers have misconceptions regarding what exactly is required to get the loans they need.

Getting Gift Funds for your down payment on a Kentucky FHA Mortgage.

What is the Great Way to do it?

To avoid getting turn down for your Kentucky FHA mortgage loan if you are getting a gift from your mom, dad or another family member, please follow these rules:

The source of the down payment must always show FHA gift funds and their source (usually a relative). It cannot be a personal loan or cash.

Common Gift Fund Issues:

Scenario 1 – only gift funds being used in transaction Gift amount: $5,000

Common submission problem:

Source of down payment submitted as “checking and savings account.”

Asset submitted as “checking account” with the financial institution as “Gift from Relative.”

Correct submission practice:

Source of down payment should be submitted as an “FHA Gift from relative for $5,000”

If funds are not yet in the bank account, DU should be submitted as…

Yesterday you may have read the blog post on questions to ask yourself before applying for a mortgage. Here are 5 additional that you may want to think about before you go into your meeting with your loan officer.

Yesterday you may have read the blog post on questions to ask yourself before applying for a mortgage. Here are 5 additional that you may want to think about before you go into your meeting with your loan officer.