What It Is and Why You Should Care for a Kentucky Mortgage Loan Approval

Think back to the last time you financed a purchase — be it a home, automobile, or what have you… You may remember having heard the term “debt-to-income ratio.” Today I want to spend some time going over exactly what this ratio is, and to also touch on how it can effect your personal finances.

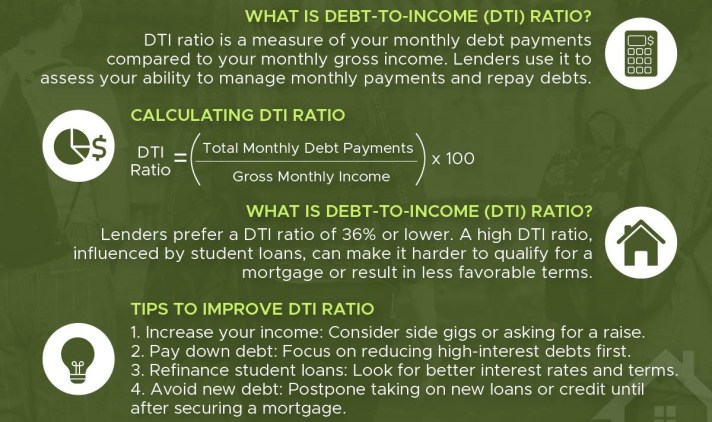

What is your debt-to-income ratio?

Commonly referred to as your “DTI,” your debt-to-income ratio is a personal finance benchmark that relates your monthly debt payments to your monthly gross income.

As an example… Let’s say that your gross monthly salary is $5,000 and you are spending $2,800 of it toward monthly debt payments. In that case, your DTI would be an unhealthy 56%.

This version of your DTI is sometimes referred to as your “back-end” DTI. This is often broken down further to give a front-end debt-to-income ratio, which is a component of your back-end DTI.

How to calculate your front-end Debt to income ratio for a Kentucky Mortgage Loan Approval

Your front-end DTI is calculated by dividing your monthly housing costs by your monthly gross income. Front-end DTI for renters is simply the amount paid in rent, whereas for homeowners it is the sum of mortgage principal, interest, property taxes, and home insurance (i.e., your PITI) divided by gross monthly income.

From above, if that $2,800 in debt payments is attributable to $1,500 in housing costs and $1,300 in non-housing costs, then your front-end DTI is $1,500/$5,000 = 30% (and your back-end ratio is still 56%, as calculated above).

How lenders use your DTI for a Kentucky Mortgage Loan Approval

Kentucky Mortgage lenders typically use DTI (along with other variables) to determine whether or not you qualify for a loan, and to help determine your Kentucky mortgage rate. A high front-end DTI raises red flags with lenders because it is commonly associated with borrower default. In fact, reducing front-end DTI to reduce the risk of homeowner default was one of the main objectives of the loan modification programs introduced by the government in 2009.

There are specific limits for DTI that are used as cut-off points when evaluating borrowers. Current DTI limits for conventional conforming mortgage loans are typically 28% on the front end and 36% on the back end, though these limits are slightly higher for government subsidized Kentucky FHA loans.

While there are certainly other factors to consider when determining our eligibility for financing (e.g., credit score, etc.), your DTI is an important determinant that you should be aware of. By working to improve it, you can make yourself a better credit risk, and thus get more favorable treatment from lenders.

Two obvious ways to improve DTI are to increase your income and/or decrease your debt. Both are solid goals.

Why Debt to income ratio Matters to Mortgage Lenders in Kentucky

Mortgage lenders use your DTI to assess risk. A high DTI can be a red flag that you may struggle to make payments—especially if unexpected expenses come up.

Here are general DTI guidelines across loan programs:

| Loan Type | Max Front-End DTI | Max Back-End DTI |

|---|---|---|

| Conventional | ~45% | ~45% |

| FHA | ~45% | Up to 56.99% w/ AUS |

| VA | N/A | 41% + residual income |

| USDA | ~32% | 45% |

Tip: FHA and VA loans offer more flexibility for higher DTIs, especially if you have strong compensating factors like good credit or savings.

—

| Joel LobbMortgage Broker – FHA, VA, USDA, KHC, Fannie MaeEVO Mortgage • Helping Kentucky Homebuyers Since 2001 |

Call/Text: 502-905-3708 Call/Text: 502-905-3708 Email: kentuckyloan@gmail.com Email: kentuckyloan@gmail.com Website: www.mylouisvillekentuckymortgage.com Website: www.mylouisvillekentuckymortgage.com  Address: 911 Barret Ave, Louisville, KY 40204 Address: 911 Barret Ave, Louisville, KY 40204NMLS #57916 | Company NMLS #1738461 |

| Free Info & Homebuyer Advice → |

| Kentucky Mortgage Loan ExpertFHA | VA | USDA | KHC Down Payment Assistance | Fannie MaeEqual Housing Lender. This is not a commitment to lend. All loans are subject to credit approval and program requirements. |

USDA and Rural Housing Loans are still available in mount Washington ky 40047

LikeLike

Mount Washington ky mortgage rural housing mortgage rates loan and USDA Rural are still available in 40047 ky rural housing mortgage rates approved RHS areas

LikeLike

https://www.creditkarma.com/home-loans/i/debt-to-income-ratio/

LikeLike