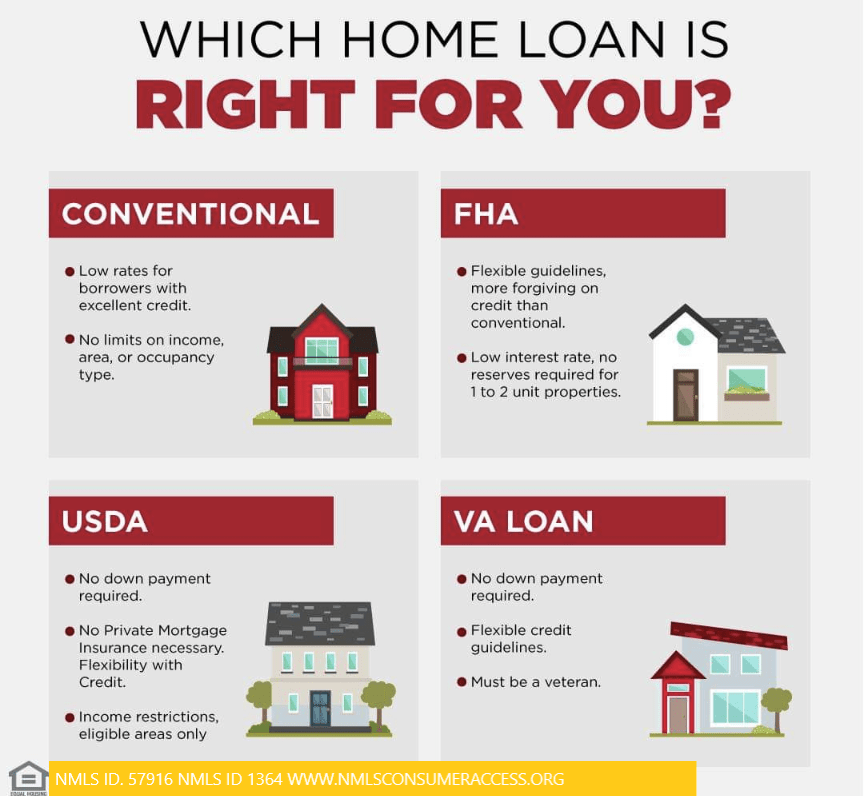

Here’s a comparison chart outlining different loan programs for first-time home-buyers in Kentucky

| Kentucky Mortgage Loan Program | Kentucky FHA Loan | Kentucky VA Loan | Kentucky USDA Loan | Kentucky Conventional Loan |

|---|---|---|---|---|

| Down Payment | 3.5% of the purchase price | Typically no down payment | 0% down payment | 3% – 20% down payment |

| Credit Score Requirement | 500-579: 10% down payment 580+: 3.5% down payment | No minimum credit score but typically 580 and above for lower credit score requirements | No minimum credit score but 640 or higher and some lenders will go down to 580 with compensating factors such as lower debt to income ratio and reserves | 620 or higher |

| Mortgage Insurance | Upfront Mortgage Insurance Premium (UFMIP) and Annual Mortgage Insurance Premium (MIP)FHA loan requires both an upfront premium of 1.75% of the loan amount and an annual premium of 0.15% to 0.75%.4 Payment of upfront premiums is at the loan issuance. | Funding Fee varies from VA funding fees for home buying range from 1.4% to 3.6% of the loan amount, while fees for a VA refinance range from 0.5% (for an IRRRL refinance) to 3.6 percent (for a repeat VA borrower using a cash-out refinance) | Guarantee Fee 1% upfront and .35 monthly fee for life of loan | Private Mortgage Insurance (PMI) may be required-Based on credit score and down payment and debt to income ratio-Not for life of loan |

| Property Eligibility | Must be primary residence | Must be primary residence | Must be in eligible rural areas and primary residence | No specific property restrictions, primary residence, second home, rentals all okay |

| Income Limits | No specific income limits, but debt-to-income ratio restrictions apply | No specific income limits for VA loans, but VA has residual income requirements | Income must not exceed 115% of the area median income-They’re are income limits-be careful on this option | Typically no income limits |

| Interest Rates | Competitive interest rates | Typically lower interest rates | Competitive interest rates | Competitive interest rates |

| Loan Limits | Yes and varies by location | VA county loan limits apply | No loan limits | Conforming loan limits apply |

First-Time Homebuyers Kentucky Mortgage Offerings to consider

Kentucky First-Time Home Buyer Loans: 100% Financing, Bad Credit, & Down Payment Assistance

Kentucky offers several loan programs. These include 100% financing options with no down payment required. The programs also offer down payment assistance and flexible credit requirements. These are available through FHA, VA, USDA, and Kentucky Housing Corporation (KHC) loans.

- 100% financing loans (no down payment required)

- Bad credit mortgage options (FHA, VA, USDA, KHC)

- Down payment assistance programs (up to $10,000+ in help)

- Income limits & property requirements

- How to qualify after bankruptcy or foreclosure

Kentucky First-Time Home Buyer Loan Programs

1. 100% Financing Loans (No Down Payment Required)

If you don’t have savings for a down payment, these Kentucky loans can help:

USDA Loans For rural and suburban areas (no down payment, low mortgage insurance).

VA Loans For veterans & active military (no down payment, no monthly PMI, flexible credit).

KHC No Down Payment Loan Kentucky Housing Corporation offers conventional loans with 100% financing.

2. FHA Loans (Low Down Payment & Bad Credit Approval)

Minimum credit score: 580 (3.5% down) or 500 (10% down).

Down payment: As low as 3.5%.

Bankruptcy/Foreclosure: Eligible after 2-3 years (exceptions possible).

3. Kentucky Housing Corporation (KHC) Loans

KHC offers down payment assistance. They also provide low-interest mortgages:

Down Payment Assistance (DAP): Up to $12,500

Credit score minimum: Typically 620.

4. There are several Down Payment Assistance Programs in Kentucky.

These programs offer coverage for closing costs. They also provide support for down payments. KHC DAP offers up to $10,000. FHA Gift Funds allow family or employer to gift the down payment.

Local Grants Check with your city/county for first-time buyer aid.

Kentucky Home Buyer Requirements

Income Limits

USDA Varies by county (typically up to 115% of area median income).

KHC varies by program higher with secondary market and MRB income limits with lower household limits

FHA/VA No strict income caps, but debt-to-income (DTI) must be below certain thresholds

Property Requirements

FHA properties must meet safety standards. Each appraisal must be done by a FHA approved appraiser.

USDA properties must be in an eligible rural area. A FHA approved appraisal is required. Condos must be on the FHA approved list and meet FHA minimum standards.

KHC Must be a primary residence (no investment properties).

Bankruptcy & Foreclosure Waiting Periods for Kentucky Mortgage Loans

| Loan Type | Chapter 7 Bankruptcy | Chapter 13 Bankruptcy | Foreclosure |

|---|---|---|---|

| FHA | 2 years from discharge | 1 year of on-time payments with court approval | 3 years from foreclosure date |

| VA | 2 years from discharge | 1 year of on-time payments with court approval | 2 years from foreclosure date |

| USDA | 3 years from discharge | 1 year of on-time payments with court approval | 3 years from foreclosure date |

| Conventional (Fannie/Freddie) | 4 years from discharge | 2 years from discharge if hardship shown (rare exception) | 7 years from foreclosure (can be 3 if extenuating) |

Discharged dates use to qualify on the seasoning of Chapter 7 And Chapter 13 and Foreclosure

- Chapter 7: A full discharge of debts. Most loans start the waiting period from the discharge date, not the file date.

- Chapter 13: You can qualify while still in the plan, after 12 months of on-time payments and with court approval.

- Foreclosure: Waiting period starts from the sheriff sale or deed transfer date, not when you stopped paying.

What Lenders Will Want to See after a bankruptcy or foreclosure

- Re-established credit with on-time payments since discharge/foreclosure

- Solid employment history (2 years preferred)

- Explanation letter (LOE) showing financial stability and what caused the event

Waiting periods to qualify for a mortgage loan in Kentucky

- Here are the waiting periods to qualify for a mortgage loan in Kentucky. These are after a bankruptcy or foreclosure. The information is updated for 2025.

- FHA – Buy again in 2-3 years

VA – Buy again in 2 years

USDA – Buy again in 3 years

Conventional – Buy again in 4-7 years

Joel has worked with KHC for 20 of his 22 years in the mortgage lending business. Joel said, “A lot of my clients would not have been able to purchase a home of their own. They might have delayed their purchase due to the lack of a down payment. However, with the $10,000 DAP loan program, they get into a house sooner. This starts their path to homeownership while building equity instead of throwing their money away.”

When you’re ready to purchase a home in Joel’s area, contact him at:

Text or call: 502-905-3708

Email: Kentuckyloan@gmail.com

Website: www.mylouisvillekentuckymortgage.com

Any questions, please don’t hesitate to reach out via, text, email, or call. Advice is always free.

One of Kentucky’s highest rated mortgage loan officers for FHA, VA, USDA, Kentucky Housing KHC and conventional mortgage loans.

Joel Lobb Mortgage Loan Officer NMLS 57916

EVO Mortgage

911 Barret Ave, Louisville, KY 40204

Company NMLS ID # 173846

Text/call: 502-905-3708

email: kentuckyloan@gmail.com

http://www.mylouisvillekentuckymortgage.com/

NMLS 57916 | Company NMLS #173846

The view and opinions stated on this website belong solely to the authors, and are intended for informational purposes only. The posted information does not guarantee approval, nor does it comprise full underwriting guidelines. This does not represent being part of a government agency. The views expressed on this post are mine and do not necessarily reflect the view of my employer. Not all products or services mentioned on this site may fit all people.

(www.nmlsconsumeraccess.org).

Kentucky First Time Homebuyers FHA, VA, USDA & Rural Housing, KHC and Fannie Mae mortgage loans