Can you use Foster Income for a Kentucky Mortgage Loan Approval? … Foster Income for a Kentucky Mortgage Yes, if it can be documented that foster care income

Can Foster Income Be Used for a Kentucky Mortgage Loan Approval?

Yes, foster income may be used to qualify for a Kentucky mortgage loan, but it must be properly documented, stable, and acceptable under the loan program being used.

For Kentucky homebuyers, foster care income can sometimes make a major difference in mortgage approval. The key issue is not simply whether the borrower receives the income. The real question is whether the lender can document the income, verify a history of receiving it, and show that it is likely to continue.

Can Foster Care Income Count Toward Mortgage Approval?

In many cases, yes. Foster care income may be considered qualifying income for FHA, VA, USDA, KHC, and conventional mortgage loans when the income meets the applicable underwriting guidelines.

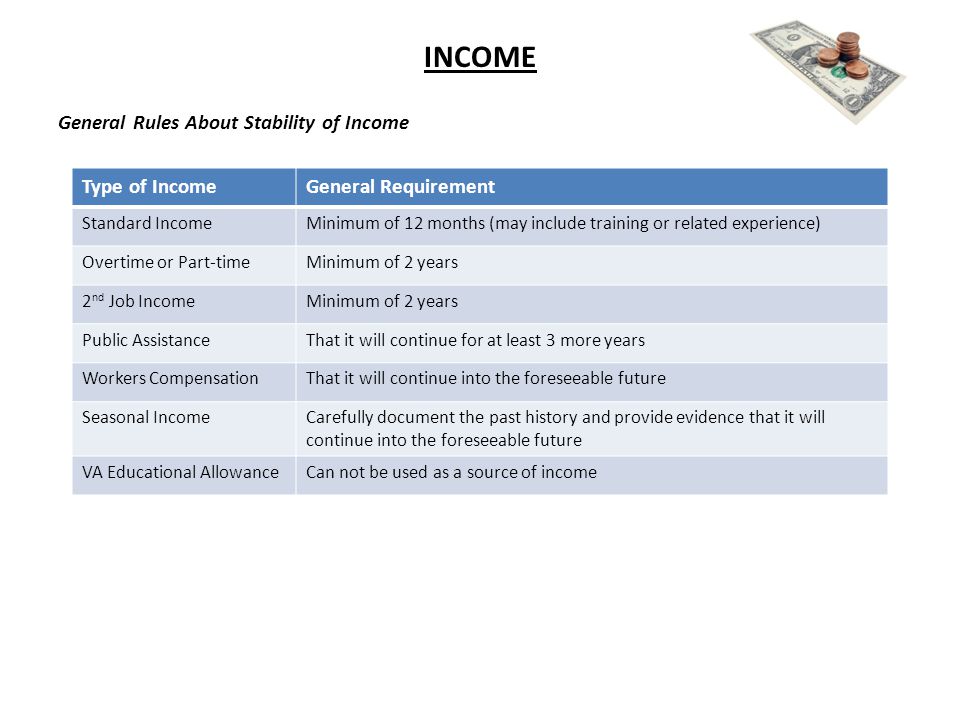

Most mortgage programs look at four main factors:

- How long the borrower has received foster income

- Whether the income is documented through an agency, county, or state source

- Whether the payments are stable or reasonably consistent

- Whether the income is likely to continue

This is why foster income should be reviewed before a full mortgage application is submitted. A lender needs to verify how the income is paid, how long it has been received, and whether it can be used under the specific loan program.

Foster Income Documentation Usually Needed

To use foster income for a Kentucky mortgage loan approval, borrowers should be prepared to provide documentation such as:

- A letter from the state, county, or foster care agency showing the payment amount

- Proof of how often the income is paid

- Recent bank statements showing deposits of the foster income

- A history of receiving the income, often 12 to 24 months depending on the loan program

- Documentation showing whether the income is expected to continue

Because foster care payments may not always appear as taxable income on a federal tax return, bank statements and agency letters are often very important. Under federal tax rules, qualified foster care payments are generally excluded from gross income, so the mortgage lender may need alternative documentation to prove the income.

Foster Income and Conventional Loans

For conventional mortgage loans, foster-care income may be used when it is properly documented. Fannie Mae generally expects a two-year history of providing foster care services. However, if the borrower has at least a 12-month history, the income may still be considered stable if it does not represent more than 30% of the total gross qualifying income.

This can help Kentucky buyers who receive foster income but have not yet received it for a full two years. The stronger the documentation, the better the file.

Foster Income and FHA Loans

FHA loans may allow foster care income when it is stable and properly documented. FHA underwriting typically focuses on whether the income has been received consistently and whether it is likely to continue.

For FHA buyers in Kentucky, the safest approach is to document the income with agency letters and bank statements showing a clear history of deposits. If the foster income is a large part of the borrower’s qualifying income, the underwriter may review it more closely.

Foster Income and USDA Loans in Kentucky

USDA Rural Housing loans are popular in Kentucky because they offer zero-down financing in eligible rural and suburban areas. USDA looks for stable and dependable income used to repay the mortgage.

For USDA approval, the lender generally needs to document the income source, verify the history of receiving the income, and establish that the income is likely to continue for at least three years when it is used for repayment income.

Foster Income and VA Loans

VA loans may also consider foster income when the income is verifiable, stable, reliable, and expected to continue. VA underwriting focuses heavily on whether the veteran or eligible borrower has enough stable income to repay the mortgage after considering debts, household expenses, and residual income requirements.

For Kentucky veterans using foster income, the file should clearly show where the income comes from, how much is received, and whether it is expected to continue.

Foster Income and KHC Loans

Kentucky Housing Corporation, also known as KHC, may be used with FHA, VA, USDA, or conventional first mortgage options depending on the borrower’s qualifications. KHC loans may also offer down payment assistance to eligible Kentucky homebuyers.

When foster income is being used on a KHC loan, the income must meet the underlying loan program requirements. For example, if the KHC first mortgage is FHA, then FHA income rules apply. If the KHC loan is conventional, then conventional income rules apply.

Common Problems With Foster Income on a Mortgage Application

Foster income can be useful, but there are several issues that can create underwriting problems:

- The borrower cannot document a clear payment history

- The income has only been received for a short period of time

- The income varies significantly from month to month

- The foster placement may not continue long enough

- The income is not deposited into a bank account

- The borrower does not have a letter from the paying agency

The best strategy is to review the foster income before shopping for homes. That way, the pre-approval is based on income the lender can actually use.

Example: How Foster Income Can Help a Kentucky Buyer Qualify

Assume a Kentucky homebuyer earns $4,500 per month from employment and receives $900 per month in documented foster care income. If the lender can use the foster income, the borrower’s qualifying income may increase from $4,500 to $5,400 per month.

That additional income can improve the debt-to-income ratio and may help the buyer qualify for a higher purchase price or a stronger loan approval.

However, if the foster income cannot be documented or is not expected to continue, the lender may not be able to use it.

Bottom Line

Foster income can potentially be used for a Kentucky mortgage loan approval, but documentation is everything. The lender must be able to verify the payment amount, history, and stability of the income.

If you are a Kentucky homebuyer receiving foster care income, the best move is to have the income reviewed early before you make an offer on a home.

Kentucky Mortgage Help

Have questions about using foster income, FHA loans, VA loans, USDA loans, KHC down payment assistance, or conventional mortgage approval in Kentucky?

Call or text Joel Lobb today at 502-905-3708.

You can also email kentuckyloan@gmail.com.

Joel Lobb

Mortgage Loan Officer

NMLS #57916

EVO Mortgage

Company NMLS #1738461

Equal Housing Lender

This is not a commitment to lend. All loans are subject to credit approval, income verification, property approval, program guidelines, and underwriting requirements. Not affiliated with HUD, FHA, VA, USDA, Kentucky Housing Corporation, or any government agency.

Frequently Asked Questions About Foster Income and Kentucky Mortgage Loans

Can foster care income be used to qualify for a mortgage?

Yes, foster care income may be used to qualify for a mortgage if it is properly documented and meets the loan program’s stability and continuance requirements.

Does foster income have to be on my tax return?

Not always. Qualified foster care payments may be excluded from taxable income, so they may not appear as taxable income on a federal tax return. Mortgage lenders may need agency letters and bank statements to verify the income.

How long do I need to receive foster income before using it for mortgage approval?

It depends on the loan program. Some programs may require a longer history, while conventional guidelines may allow foster income with at least 12 months in certain cases if it is not more than 30% of the total qualifying income.

Can foster income be used for an FHA loan in Kentucky?

Foster income may be considered for FHA mortgage approval when it is stable, documented, and acceptable to underwriting.

Can foster income be used for a USDA loan in Kentucky?

Foster income may be considered for USDA approval if it is stable, dependable, documented, and expected to continue under USDA income guidelines.

Can foster income help me qualify for KHC down payment assistance?

Possibly. KHC loans follow the income requirements of the underlying first mortgage program, such as FHA, VA, USDA, or conventional financing.

{ “@context”: “https://schema.org”, “@graph”: [ { “@type”: “Article”, “@id”: “https://kyfirsttimehomebuyer.wordpress.com/foster-income-kentucky-mortgage-loan-approval/#article”, “headline”: “Can Foster Income Be Used for a Kentucky Mortgage Loan Approval?”, “description”: “Learn whether foster care income can be used to qualify for a Kentucky mortgage loan, including FHA, VA, USDA, KHC, and conventional loan options.”, “author”: { “@type”: “Person”, “name”: “Joel Lobb, Mortgage Broker FHA, VA, KHC, USDA”, “url”: “https://www.mylouisvillekentuckymortgage.com/” }, “publisher”: { “@type”: “Organization”, “name”: “Joel Lobb, Mortgage Broker FHA, VA, KHC, USDA”, “url”: “https://www.mylouisvillekentuckymortgage.com/” }, “mainEntityOfPage”: { “@type”: “WebPage”, “@id”: “https://kyfirsttimehomebuyer.wordpress.com/foster-income-kentucky-mortgage-loan-approval/” } }, { “@type”: “FAQPage”, “@id”: “https://kyfirsttimehomebuyer.wordpress.com/foster-income-kentucky-mortgage-loan-approval/#faq”, “mainEntity”: [ { “@type”: “Question”, “name”: “Can foster care income be used to qualify for a mortgage?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Yes, foster care income may be used to qualify for a mortgage if it is properly documented and meets the loan program’s stability and continuance requirements.” } }, { “@type”: “Question”, “name”: “Does foster income have to be on my tax return?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Not always. Qualified foster care payments may be excluded from taxable income, so mortgage lenders may use agency letters and bank statements to verify the income.” } }, { “@type”: “Question”, “name”: “Can foster income be used for FHA, VA, USDA, KHC, and conventional loans?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Possibly. Foster income may be used if it meets the documentation, stability, history, and continuance requirements for the specific mortgage program.” } } ] }, { “@type”: “BreadcrumbList”, “@id”: “https://kyfirsttimehomebuyer.wordpress.com/foster-income-kentucky-mortgage-loan-approval/#breadcrumb”, “itemListElement”: [ { “@type”: “ListItem”, “position”: 1, “name”: “Kentucky First Time Home Buyer”, “item”: “https://kyfirsttimehomebuyer.wordpress.com/” }, { “@type”: “ListItem”, “position”: 2, “name”: “Foster Income for Kentucky Mortgage Loan Approval”, “item”: “https://kyfirsttimehomebuyer.wordpress.com/foster-income-kentucky-mortgage-loan-approval/” } ] } ] }