Updated June 17, 2026 · Kentucky First-Time Home Buyer Guide

Kentucky First-Time Home Buyer Programs 2026: FHA, VA, USDA, Conventional and KHC Down Payment Assistance

Compare Kentucky mortgage options, down payment assistance, credit score guidelines, zero-down loans, and realistic next steps before you start shopping for a home.

Buying your first home in Kentucky can feel overwhelming. Down payment, closing costs, credit scores, income limits, inspections, appraisals, property rules and lender paperwork can all hit at once. The good news is that Kentucky buyers have several strong mortgage options in 2026, including VA zero-down loans, USDA zero-down loans, FHA low-down-payment loans, conventional 3% down loans, and Kentucky Housing Corporation down payment assistance.

My name is Joel Lobb, Senior Loan Officer, NMLS #57916. I help Kentucky home buyers compare mortgage programs, estimate payments, review down payment assistance options, and choose the loan structure that fits their credit, income, property location, and cash-to-close goals.

Need a Kentucky mortgage pre-approval?

Call or text 502-905-3708, email kentuckyloan@gmail.com, or start your secure online application here.

Quick Navigation

- Best Kentucky first-time buyer programs

- Program comparison chart

- KHC down payment assistance

- FHA loans in Kentucky

- USDA Rural Housing loans

- VA loans for Kentucky veterans

- Conventional 3% down loans

- Mortgage payment calculator

- Step-by-step home buying process

- Frequently asked questions

Best Kentucky First-Time Home Buyer Programs in 2026

There is no single best mortgage program for every Kentucky buyer. The right loan depends on your credit score, income, monthly debts, property location, military eligibility, household size, and how much money you have available for down payment and closing costs.

KHC Down Payment Assistance

Kentucky Housing Corporation assistance may help eligible buyers cover down payment, closing costs, and prepaid expenses when paired with a KHC first mortgage.

FHA Loan

FHA loans are often useful for buyers with limited savings, higher debt-to-income ratios, or less-than-perfect credit. FHA commonly allows 3.5% down with qualifying credit.

USDA Rural Housing Loan

USDA Rural Housing may allow 100% financing for eligible borrowers and eligible properties. Many small towns and suburban areas in Kentucky may qualify.

VA Loan

VA loans are one of the strongest mortgage options for eligible veterans, active-duty service members, qualifying National Guard or Reserve members, and certain surviving spouses.

Conventional 3% Down Loan

Conventional 3% down options may work well for buyers with stronger credit, stable income, and enough funds for down payment and closing costs.

Local Kentucky tip: The best loan is not always the lowest interest rate on paper. Mortgage insurance, down payment assistance, seller-paid closing costs, appraisal rules, KHC second mortgage payments, and future refinance options can all change the real cost of the loan.

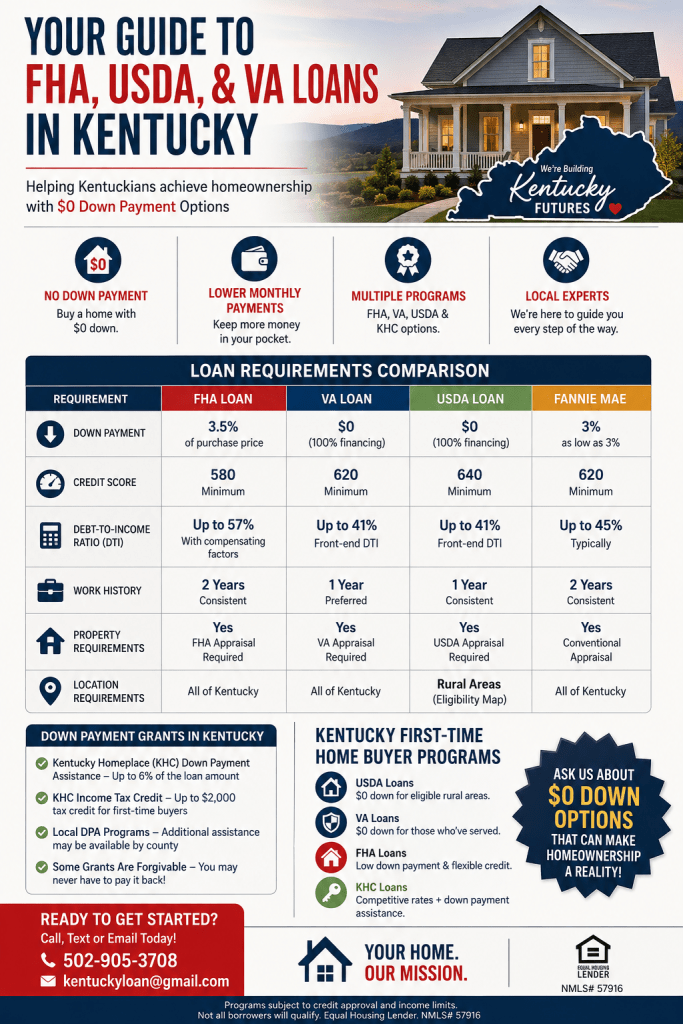

Kentucky First-Time Buyer Program Comparison Chart

Use this chart as a starting point. Final approval depends on credit, income, assets, property type, appraisal, underwriting, investor guidelines, and program availability.

| Program | Typical Down Payment | Credit Score Notes | Best For |

|---|---|---|---|

| KHC with DAP | Varies by first mortgage; assistance may help with cash to close | KHC generally lists 620 minimum credit score for major program categories; some conventional options may require 660 | Buyers who qualify for a KHC first mortgage and need down payment or closing cost help |

| FHA | 3.5% minimum with qualifying credit | FHA allows flexible credit; lender overlays may apply | Buyers with limited savings, credit challenges, or higher debt-to-income ratios |

| USDA Rural Housing | 0% down for eligible properties and borrowers | Many lenders prefer 620 to 640+, with automated approval preferred | Buyers in eligible rural or suburban Kentucky areas |

| VA | 0% down for eligible borrowers | VA does not set one universal minimum credit score, but lenders may have overlays | Eligible veterans, active-duty military, National Guard, Reserve members, and surviving spouses |

| Conventional 3% Down | 3% down for eligible first-time buyers | Often stronger with 660+ to 720+ credit depending on pricing and approval | Buyers with stronger credit who want conventional financing |

KHC Down Payment Assistance in Kentucky

Kentucky Housing Corporation, often called KHC, offers affordable mortgage programs and down payment assistance for eligible Kentucky buyers. KHC assistance can help with down payment, closing costs, and prepaid expenses when paired with an eligible KHC first mortgage.

Current KHC Regular DAP Snapshot

- Assistance may be available up to $12,500 in $100 increments.

- Repayable over a 15-year term.

- Current KHC DAP page lists the DAP rate at 4.75%.

- Available to KHC first-mortgage recipients when program guidelines are met.

- KHC eligibility pages list a 620 minimum credit score for major KHC program categories.

Important KHC limit note: KHC pages may show different purchase price references depending on whether you are reviewing the first mortgage page or the DAP page. Do not write an offer based only on a blog post. The correct limit needs to be verified through a KHC-approved lender at the time of pre-approval.

Helpful official KHC links:

- KHC Down Payment Assistance

- KHC Loan Programs

- KHC Eligibility Requirements

- KHC Current Interest Rates

- Kentucky $12,500 Down Payment Assistance 2026 Guide

FHA Loans for Kentucky First-Time Home Buyers

FHA loans remain one of the most common mortgage options for Kentucky first-time buyers because they combine a low down payment with flexible underwriting compared to many conventional loan programs.

Why Kentucky buyers choose FHA

- Low down payment: FHA commonly allows 3.5% down with qualifying credit.

- Flexible credit profile: FHA may work for buyers rebuilding credit, depending on automated underwriting and lender requirements.

- Seller-paid closing costs: FHA allows seller concessions within program limits, which may help reduce cash needed at closing.

- KHC compatibility: KHC lists FHA as one of its available first mortgage options when KHC guidelines are met.

FHA loans include upfront and monthly mortgage insurance. A realistic FHA payment estimate should include principal, interest, property taxes, homeowners insurance, FHA mortgage insurance, HOA dues if applicable, and any KHC second mortgage payment if down payment assistance is used.

Look up official FHA mortgage limits by county

USDA Rural Housing Loans in Kentucky

USDA Rural Housing can be one of the best first-time home buyer programs in Kentucky because it may allow 100% financing for eligible borrowers and eligible properties. USDA is not just for farmland. Many smaller towns and suburban areas may qualify depending on the USDA property eligibility map.

USDA loan advantages

- 0% down payment for eligible buyers and eligible properties.

- Often lower monthly mortgage insurance than FHA.

- Useful in many rural and suburban Kentucky communities.

- Can sometimes be combined with approved assistance structures when guidelines allow.

USDA eligibility has two major parts: property eligibility and household income eligibility. The USDA map is a starting point, not a final loan approval. Final eligibility is determined during the mortgage application and underwriting process.

Check official USDA property eligibility

Learn more about Kentucky USDA Rural Housing loans

VA Loans for Kentucky Veterans and Military Buyers

For eligible borrowers, the VA home loan is often one of the strongest mortgage programs available. Kentucky veterans, active-duty service members, National Guard members, Reserve members, and eligible surviving spouses may be able to purchase with zero down using VA financing.

VA loan benefits

- 0% down payment for eligible borrowers.

- No monthly mortgage insurance.

- Competitive fixed-rate options.

- Flexible refinance options later, including VA IRRRL for eligible existing VA loans.

VA loans may include a one-time VA funding fee unless the borrower qualifies for an exemption. The VA explains that the funding fee can often be financed into the loan or paid at closing.

View official VA funding fee and closing cost information

Read the Kentucky VA mortgage FAQ

Conventional 3% Down Loans for Kentucky Buyers

Conventional loans can work well for first-time buyers with stronger credit, stable income, and enough funds for down payment and closing costs. Some conventional programs allow as little as 3% down for eligible first-time buyers.

KHC also lists conventional options such as HFA Preferred, HFA Preferred Plus 80, and Freddie HFA Advantage. These programs may allow a 3% down payment, KHC DAP compatibility, no minimum borrower contribution, and no reserve requirements when guidelines are met.

Conventional loans can be attractive because private mortgage insurance may be cancellable later when equity and payment history requirements are met. However, conventional pricing and mortgage insurance are sensitive to credit score, debt-to-income ratio, property type, and down payment.

Compare Kentucky USDA, FHA, VA, conventional and KHC loan programs

Kentucky Mortgage Payment Calculator

Before you choose a loan program, estimate the full monthly mortgage payment. A realistic Kentucky mortgage payment includes more than principal and interest.

Use this payment checklist

- Principal and interest

- County property taxes

- Homeowners insurance

- FHA MIP, USDA annual fee, VA funding fee impact, or conventional PMI when applicable

- HOA dues, if the property has an HOA

- KHC second mortgage payment, if using repayable down payment assistance

Open the Kentucky Mortgage Payment Calculator

How to Get a Kentucky Mortgage Quote Without Guesswork

A good mortgage quote should compare the full cost of the loan, not just the interest rate. When I review a quote for a Kentucky buyer, I look at rate, APR, discount points, lender fees, mortgage insurance, escrow estimates, seller credits, down payment assistance, and whether the program truly fits the property and borrower.

For the most accurate quote, be ready to share:

- Estimated credit score range

- County and city where you plan to buy

- Target purchase price

- Estimated household income

- Monthly debts from the credit report

- Available savings for down payment, closing costs, and reserves

- Military eligibility, if applicable

Need a second opinion on a loan estimate?

Call or text 502-905-3708 or email kentuckyloan@gmail.com.

Step-by-Step Kentucky First-Time Home Buyer Process

- Check your credit and budget. Review your credit score range, monthly debts, income, savings, and comfort-level payment before you shop.

- Get pre-approved. A real pre-approval should review income, assets, credit, and debt-to-income ratio.

- Compare FHA, VA, USDA, conventional, and KHC. The best program depends on eligibility, payment, cash to close, and property type.

- Choose a Kentucky real estate agent. Work with an agent who understands FHA, VA, USDA, and KHC property requirements.

- Write an offer with the right financing terms. Seller concessions, inspection timelines, repair terms, and appraisal requirements can affect the deal.

- Complete underwriting. Your lender verifies documentation, orders the appraisal, clears conditions, and prepares closing.

- Close and move in. Review your final Closing Disclosure, bring verified funds if needed, and sign final documents.

Serving First-Time Home Buyers Across Kentucky

I help buyers throughout Kentucky, including Louisville, Lexington, Bowling Green, Owensboro, Covington, Florence, Richmond, Elizabethtown, Georgetown, Shelbyville, Shepherdsville, Paducah, Frankfort, Nicholasville, Radcliff, Hopkinsville, and all 120 Kentucky counties.

Popular county searches include Jefferson County first-time home buyer programs, Fayette County FHA loans, Warren County USDA loans, Boone County VA loans, Kenton County KHC assistance, Hardin County zero-down mortgages, and Bullitt County down payment assistance.

Frequently Asked Questions About Kentucky First-Time Home Buyer Programs

What is the best first-time home buyer program in Kentucky?

The best program depends on your situation. VA may be best for eligible military borrowers, USDA may be best for eligible rural or suburban properties, FHA may fit buyers who need flexible credit guidelines, KHC may help with cash to close, and conventional 3% down may be strong for buyers with better credit.

How much down payment do I need to buy a house in Kentucky?

Some eligible Kentucky buyers may qualify for 0% down with VA or USDA. FHA commonly requires 3.5% down with qualifying credit. Conventional first-time buyer programs may allow 3% down. KHC assistance may help eligible buyers reduce cash needed at closing.

Does Kentucky have down payment assistance?

Yes. Kentucky Housing Corporation offers down payment assistance for eligible borrowers using KHC first mortgage programs. KHC’s Regular DAP page currently lists assistance up to $12,500, subject to program rules and approval.

What credit score do I need for KHC in Kentucky?

KHC’s eligibility page lists a 620 minimum credit score for major KHC program categories. Some specific conventional options may require higher scores. Your lender must verify current guidelines, investor overlays, and automated underwriting approval.

Can I use KHC with FHA, VA, or USDA?

KHC lists FHA, VA, and RHS/USDA loan options in its program materials, and KHC DAP may be applicable when KHC guidelines are met. Final eligibility depends on the first mortgage, income limits, property type, purchase price, credit score, and underwriting approval.

Can I buy a home in Kentucky with student loans?

Yes, many buyers qualify with student loans. The key issue is how the mortgage program calculates the student loan payment for debt-to-income ratio. FHA, VA, USDA, and conventional loans each have their own student loan calculation rules.

How long does it take to close on a house in Kentucky?

Many Kentucky purchases close in about 30 to 45 days, but timing depends on appraisal, title work, underwriting, KHC compliance review if applicable, and USDA review if using USDA financing.

Can the seller pay my closing costs?

Often, yes. Seller-paid closing costs depend on the loan program, down payment, occupancy, and contract terms. FHA, VA, USDA, and conventional loans each have seller concession limits.

Ready to Compare Kentucky Home Buyer Programs?

If you are buying a home in Kentucky in 2026, the smartest first step is to compare your real options before you fall in love with a house. I can review FHA, VA, USDA, conventional, and KHC assistance options and help you understand the estimated payment and cash needed to close.

Joel Lobb

Senior Loan Officer | NMLS #57916

EVO Mortgage | NMLS #1738461

Licensed in Kentucky

Call/Text: 502-905-3708

Email: kentuckyloan@gmail.com

Apply online: Start a free Kentucky mortgage pre-approval

Important disclosure: This article is for informational purposes only and is not a commitment to lend. All loans are subject to credit approval, underwriting guidelines, property eligibility, investor requirements, and program availability. Rates, fees, limits, and assistance programs may change without notice. This website is not affiliated with FHA, VA, USDA, HUD, Kentucky Housing Corporation, Fannie Mae, Freddie Mac, or any government agency. Equal Housing Lender. Licensing information is available at NMLS Consumer Access.